Business

Absa Bank Kenya: The Lender That Declares War On Its Own Clients

How a bank that borrowed its own logo from a rebrand turned ruthless acceleration clauses, insider fraud, leaked customer data, and a Senate summons into a one-stop scandal dossier that should frighten every borrower in Kenya

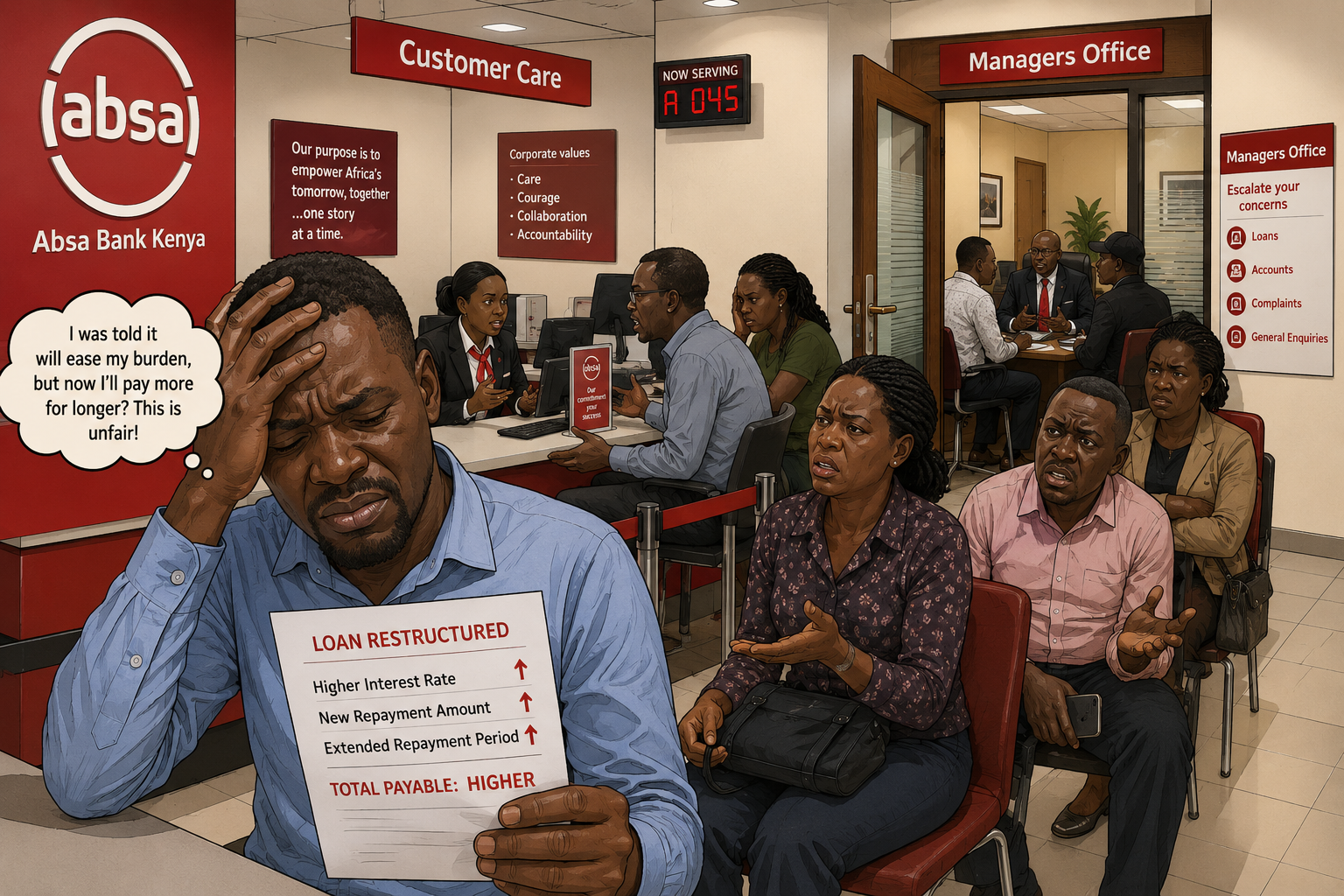

John Maina Kinyua is not a reckless borrower. He is precisely the kind of client a bank markets its long-term products to: a property owner with income-generating assets in Sigona, Kiambu County, willing to commit to 180 monthly installments stretching fifteen years into the future. He took an Sh80 million facility from Absa Bank Kenya in September 2024. He pledged two rental properties, Sigona/1294 and Sigona/2103, as security. The repayment schedule was modest: Sh180,000 every month until July 2039. Then he missed one payment in April 2025.

What followed next is a story not about a borrower in crisis. It is a story about a bank that treats its own clients like adversaries the moment a contractual technicality presents itself, and about a pattern of institutional conduct that Kenyan courts, parliamentarians, and now borrowers themselves are increasingly calling out for what it is: predatory, reckless, and in multiple documented cases, outright unlawful.

“The respondent cannot disown its own entries.” High Court of Kenya, on Absa’s pursuit of foreclosure despite its own records confirming the account had been fully regularised.

One Missed Payment. Sh79.9 Million Demanded. Fourteen Years Collapsed.

The facts in the Kinyua matter are not in serious dispute. On May 12, 2025, barely seven months after the loan was disbursed, Absa issued a 90-day statutory notice demanding immediate repayment of the entire Sh79.9 million outstanding balance. Not the arrears. Not the overdue installment. The whole loan. The bank argued, as it consistently does in such disputes, that the charge instrument gave it the unilateral right to recall the full facility the moment any default occurred.

Kinyua cleared the arrears. Absa’s own bank statements, produced in court, showed that by September 24, 2025, the account had been fully regularised and arrears reduced to zero. The bank then issued a 40-day notice to sell on September 3, 2025, demanding Sh79.8 million and advertising the properties for public auction. It was pressing ahead with the sale of income-generating assets on a loan that its own records showed was current.

The High Court was unsparing. In granting a temporary injunction halting the planned auction, the judge noted that Absa could not disown its own entries. The court described the pursuit of foreclosure against a now-performing, fully cured loan as a monumental triable issue, and ruled that a premature, accelerated foreclosure on a performing, fully regularised loan presents a formidable prima facie case with a high probability of success. The parties were directed to complete pre-trial steps within 14 days ahead of an expedited hearing.

That judicial language is not boilerplate. It is the bench telling Absa that it behaved in a manner that raised serious questions about the legality of its own recovery process. For a bank that manages tens of thousands of secured lending relationships across Kenya, those words carry institutional weight.

The Contractual Trap That Borrowers Sign Without Reading

The legal architecture that made this possible is worth examining because it is embedded in every long-term charge document Absa issues. The bank’s standard charge instruments contain acceleration clauses that trigger the right to demand the full outstanding balance immediately upon any event of default, however minor. Kinyua argued that the charge document required a specific event of default to be formally declared and a prior demand for arrears before the entire facility could be recalled. Absa countered that the mere fact of any default activated its right to the full sum.

The court found serious triable issues in that argument precisely because the bank was pressing ahead after the underlying default had been cured. But the deeper concern for anyone contemplating a long-term secured facility with Absa is that the bank appears to interpret its own charge documentation in the most aggressive manner available, and moves at speed. A 90-day statutory notice was issued just weeks after the alleged default. A 40-day sale notice followed months later. All of this occurred while arrears were being settled and while the facility still had over fourteen years to run.

What Absa effectively argued in court is that once a default occurs, cure does not matter. The clock for full acceleration has already started. The income from the very properties securing the loan, rental income that was actively servicing the debt, was about to be destroyed by the very auction that would trigger tenant flight. The court accepted the borrower’s argument about that vicious cycle explicitly. It is difficult to read the bank’s position as anything other than a strategy designed to seize valuable security at the earliest contractual opportunity, regardless of the commercial reality on the ground.

This Is Not a One-Off. Absa Has a Pattern.

The Kinyua case does not exist in isolation. It is the latest chapter in a documented institutional habit at Absa Bank Kenya that stretches back years and spans multiple product lines, client categories, and judicial forums. The pattern is consistent: move fast on security realization, resist accommodation, and lean on contractual language even when the equities point in the opposite direction.

Consider New Mega Africa Limited, a Nairobi transport company that ships clinker between Kenya and Uganda. It borrowed from Absa and charged a prime property in Kitusuru, Nairobi, as security for facilities that eventually reached Sh86.4 million. When the relationship soured, the company filed suit in the High Court in Mombasa alleging that Absa had printed its confidential financial statements without authority and shared them with third parties, exposing the firm to financial sabotage and cancellation of insurance policies. The company claimed Sh1.5 billion in damages.

In November 2022, the court entered interlocutory judgment against Absa after the bank failed to file a defence within the stipulated period. The bank then contested that judgment, arguing that no data breach had occurred and characterising the lawsuit as an attempt by the transport firm to evade its loan obligations. Absa simultaneously moved to auction the Kitusuru property to recover the outstanding debt. In June 2023, Justice Mongare issued a temporary injunction halting the auction, barring the bank from selling or transferring the property pending determination of the full case. In January 2025, Absa suffered a further setback when the High Court in Mombasa allowed a former employee to testify as a witness in the case, reopening the evidentiary record the bank had fought to keep closed.

The New Mega Africa litigation has now run for more than three years. The bank is fighting simultaneously to disclaim liability for the alleged data breach, to enforce its auction rights on the Kitusuru property, and to resist a Sh1.5 billion damages award. Those three fronts are not coincidental. They reflect a bank that moved to liquidate security while a major counter-claim was actively being litigated, a move courts have now repeatedly restrained.

Senators demanded Absa’s CEO appear before Parliament to answer for a fraud syndicate targeting retirees at Absa branches. The National Treasury Cabinet Secretary confirmed collusion between pension officers and banking staff.

Parliament Summons Absa’s CEO Over Retiree Robbery Syndicate

The courtroom is not the only arena where Absa’s conduct has attracted institutional scrutiny. In December 2025, Kenya’s Senate erupted over a fraud syndicate that was systematically targeting retirees moments after they received lump-sum pension payouts deposited into Absa Bank accounts. Senator Eddy Oketch of Migori tabled a statement before the Senate Finance and Budget Committee demanding a full accounting of fraud cases involving Absa accounts since 2022 and the status of investigations into each of them.

The cases were not abstract. Senators cited a retired teacher who lost her entire pension payout of Sh2.4 million from an Absa account. A retired police officer was robbed of cash moments after leaving an Absa branch, with senators raising concerns that insiders were feeding withdrawal information to criminal networks operating outside the bank. Nyamira Senator Okongo Omogeni went further, calling for Absa’s Chief Executive Officer, Abdi Mohamed, to appear before the Senate in person to explain how fraudsters were apparently able to monitor transactions and swiftly drain accounts after pension deposits.

The National Treasury Cabinet Secretary John Mbadi, appearing before the Senate, made a statement that should have triggered a regulatory response: he confirmed the existence of collusion between pension officers and banking staff in defrauding retirees. That admission was made about cases specifically linked to Absa accounts. The government subsequently committed to fully digitising the pension payment system from July 2025 to reduce the human interface that was enabling the fraud.

That Senate hearing did not take place in a vacuum. It came months after the Employment and Labour Relations Court upheld the dismissal of Lilian Adhiambo, former branch manager of Absa Bank’s Karen Prestige branch, after forensic investigators linked her to a syndicate that drained Sh6.3 million from customer accounts in October 2019. The court reviewed the forensic reports and found the bank’s decision to dismiss her fair and lawful. The Karen Prestige case was not an outlier. Former compliance officers have described a shadow network centered in Nairobi suburbs where rings of insiders and external fraudsters coordinate attacks on mobile banking platforms in real time.

Sh4.5 Billion: When Absa Itself Was the Victim

While Absa was pursuing small borrowers with aggressive acceleration clauses, the bank was simultaneously navigating the fallout from one of the largest alleged loan frauds in Kenyan corporate history. Prosecutors allege that between February 2017 and January 2018, industrialist Benson Sande Ndeta and an American co-accused, Charles Hills Jr., conspired to fraudulently obtain a dollar-denominated credit facility equivalent to Sh4.5 billion from Absa, then operating as Barclays Bank Kenya, by falsely representing themselves as acting on behalf of Savannah Cement Limited and presenting what prosecutors say were forged corporate guarantees, board resolutions, and security documents.

The case carries 12 criminal counts including conspiracy to commit fraud, obtaining credit by false pretences, forgery, and uttering forged documents. Ndeta and Hills failed to appear in court to take a plea and in March 2026 Milimani Senior Principal Magistrate Carolyne Mugo issued arrest warrants against both men. The warrants were extended in March 2026 after the accused continued to defy court orders. In parallel, Ndeta returned to the High Court seeking to halt the criminal prosecution entirely, but in December 2025 the High Court dismissed his constitutional petition and cleared the path for trial.

The Sh4.5 billion fraud case is instructive in a way the bank would prefer not to advertise. A lender that prides itself on contractual discipline and forensic documentation of borrower obligations was apparently deceived by forged board minutes and fabricated indemnity forms. While Absa pursues a borrower in Sigona for missing one installment of Sh180,000, it spent years absorbing the consequences of approving a nine-figure facility on the basis of documents that prosecutors say were fraudulent from the start.

Vetlab Sports Club: Absa Caught in a Governance War Over Sh26 Million

The complications did not stop there. In May 2026, Absa was dragged into a governance dispute at Nairobi’s century-old Vetlab Sports Club after rival factions of the club’s leadership accused the bank of illegally altering the signatories on the club’s main account, which held approximately Sh26 million at the time. The club’s chairman, Jared Ouko, and honorary secretary, Beatrice Kamau, filed suit at the High Court’s Commercial and Tax Division, accusing Absa of effecting the signatory changes without proper authority despite ongoing litigation over who constituted the club’s lawful board.

Court papers showed that Absa had previously resisted similar requests to change signatories during earlier phases of the same dispute, making the reversal all the more difficult to explain. The applicants alleged that bank officials indicated a court order had been used to justify the changes but that they had never been served with any such order. The dispute put Absa in the position of having potentially taken instructions from one faction of a contested leadership body, exposing member funds to risk in circumstances where no unambiguous legal authority to act had been established.

The Numbers Behind the Reputation Crisis

Absa Bank Kenya reported a net profit of Sh5.3 billion in the first quarter of 2026, down 13.8 percent from the Sh6.1 billion posted in the same period the previous year, as falling interest rates and reduced lending compressed income. Total interest income fell 10.1 percent to Sh13.5 billion. The bank’s gross non-performing loans stood at Sh44.3 billion at the close of September 2025, having grown by 20.5 percent to Sh42.5 billion during 2024. Against that backdrop, aggressive enforcement of secured lending contracts is commercially understandable. A bank sitting on Sh44 billion in bad debt has every incentive to tighten recovery processes.

What is harder to justify is the application of that tightening to a borrower who has cured a single missed installment on a facility that carries fourteen more years to maturity. The Kinyua matter is not a case of a serial defaulter or an insolvent borrower running from obligations. It is a case of a borrower who fell behind by one month, restored the account to performing status per the bank’s own records, and then watched as the bank pressed ahead with an auction anyway. The income-generating properties securing the loan were not at risk of disappearing. The tenants were paying rent. The cash flow was there. Absa chose the nuclear option.

In 2023, the bank’s predecessor entity was ordered by the High Court to pay general damages to Paul Kuria Ngugi after auctioning his land in Muguga and failing to furnish him with documents relating to the sale or to disclose the price achieved at auction. Justice Francis Tuiyott found that the bank, then known as Barclays Kenya before its rebrand to Absa in 2020, had failed to call evidence or challenge the borrower’s assertion that proper documentation was never provided. The court ordered disclosure of the auction proceeds and the amount credited to the borrower’s account. That judgment predates the rebrand but the institutional conduct it describes is continuous.

What Borrowers Must Understand Before Signing

The Kinyua case should function as a compulsory case study for anyone contemplating a secured long-term facility with Absa Bank Kenya. The charge documentation contains acceleration clauses that, on Absa’s reading, allow it to demand the full outstanding balance immediately upon any default, however minor, however brief, and however thoroughly cured. The bank’s interpretation of those clauses is aggressive. It moves within weeks of a default to issue statutory notices. It does not appear to factor in whether a workout arrangement or cure period would better serve both parties on a long-term facility with income-generating security.

The practical consequence is that a borrower who signs a fifteen-year mortgage with Absa is not actually secured for fifteen years in any meaningful sense. They are secured only for as long as every single installment lands on time. A single slip, whether caused by a bank processing delay, a personal cash flow disruption, or even a disputed debit, can trigger a process that within months places their property under auction notices. The cure period that common sense and commercial fairness would imply exists, apparently does not, unless it is explicitly negotiated into the charge document and specifically preserved against the general acceleration clause.

Potential borrowers dealing with Absa would be prudent to insist on explicit cure windows before acceleration can be triggered, stricter definitions of what constitutes a material default sufficient to activate foreclosure, and procedural requirements that compel the bank to issue a demand for specific arrears before it can recall the entire facility. Without those protections in writing, the standard Absa charge instrument appears to leave the borrower entirely exposed to the bank’s discretion. And the documented pattern suggests that discretion will not be exercised in the borrower’s favour.

A Bank That Does Not Trust Its Own Relationships

The deeper problem at Absa is cultural. A financial institution that simultaneously battles a Sh1.5 billion data breach claim in Mombasa, faces Senate demands for its CEO to explain pension fraud in its branches, has insider fraud convictions from its Karen Prestige branch, is embroiled in a Sh26 million signatory dispute at a sports club, is pursuing a Sh4.5 billion fraud prosecution against external actors who allegedly deceived its own officers with forged documents, and is in the High Court defending its decision to auction a regularised loan due in 2039 is not experiencing isolated incidents. It is experiencing a systemic failure of institutional character.

That failure has two faces. One faces outward toward borrowers: a confrontational enforcement posture that treats the first technical default as a licence to collapse an entire long-term credit relationship. The other faces inward: a vulnerability to insider misconduct and external fraud that has cost the bank hundreds of millions in direct losses and exposed clients ranging from retirees to transport companies to serious financial harm. Absa describes itself as an African bank committed to customer partnership and long-term relationships. Its conduct in court after court, and in parliamentary hearing after parliamentary hearing, suggests a more transactional and considerably less generous reality.

The High Court’s intervention in Sigona has bought John Maina Kinyua time. It has not restored the rental income disrupted, refunded the legal costs incurred, or compensated for the months of uncertainty during which his tenants may have received notice that their landlord’s properties were headed to auction. It has not changed the charge document he signed or the acceleration clauses it contains. And it has not produced from Absa a public statement acknowledging that pressing ahead with a sale process after its own bank statements showed zero arrears was anything other than optimal risk management.

Until the bank offers something more substantive than a commercial contract defense, every Kenyan considering a long-term secured loan with Absa is entitled to read the Kinyua judgment carefully. It is not just a court ruling. It is a warning issued in plain language by the institution that is supposed to be the last line of protection between a creditor’s contractual power and a borrower’s constitutional rights. The courts are doing their job. Absa would do well to examine whether its current approach is doing the bank, its clients, and the wider banking sector any credit at all.

Kenya Insights allows guest blogging, if you want to be published on Kenya’s most authoritative and accurate blog, have an expose, news TIPS, story angles, human interest stories, drop us an email on [email protected] or via Telegram

House Helps to Earn Minimum Salary of Sh18,047 Under New Law, Employers Who Refuse Face Jail

Inside The Urban Planning Cartel That Owns Nairobi

Absa Bank Kenya: The Lender That Declares War On Its Own Clients

Putin Rejects Zelensky Meeting Proposal

Burkina Faso Junta Intensifies Crackdown on Critics

Analo Was Just the Tip of the Iceberg: Alai Names Powerful Nairobi Planning Cartel Linked to City Hall

Ruto Reshuffles Military Leadership, Names Major General John Nkoimo Deputy Army Commander

SUPREMO: How Simba Arati’s Wife Is Running Kisii County From Her Home With Terror

Why Is a US Ebola Facility in Kenya Sparking Protests?

10 Million Kenyans’ Personal Data Allegedly Being Sold on Dark Web in Chilling New Cybersecurity Scare

Why Ruto’s Favourite Candidate Adan Mohammed Could Be Locked Out of the KRA Top Job

LifeCare on the Brink: SHA Fraud, Stolen Wages, and the Rotten Empire Jayesh Saini Built

Este Medical Kenya Fights American’s Explosive Complaints

Safaricom’s Sh1.4 Billion Reckoning: How Kenya’s Most Profitable Company Stole a Man’s Idea and Got Caught

The Rot Inside Absa: How Bank Insiders Are Looting Nairobi’s Customers

THE INSURER THAT TOOK YOUR PREMIUM AND FORGOT YOUR NAME: How ICEA Lion Left a Client Begging for Sh7.8 Million Across Four Months

Denial Under Duress: The Untold Collapse Threatening David Lagat’s DL Group’s Empire

Inside FAFSA Fraud: How Kenyan Cybercriminals Siphoned Millions from America’s Sh12 Billion Student Loan System

Court Confirms Safaricom Customers Data Was Sold To Betting Companies In Seven-Year Cover-Up

Betika Faces DCI Probe, Directors Arrest and License Revocation Over Massive 29.5 Million Safaricom Customers’ Data Breach

-

Investigations2 weeks ago

Investigations2 weeks agoLifeCare on the Brink: SHA Fraud, Stolen Wages, and the Rotten Empire Jayesh Saini Built

-

News2 weeks ago

News2 weeks agoEste Medical Kenya Fights American’s Explosive Complaints

-

Americas2 weeks ago

Americas2 weeks agoInside FAFSA Fraud: How Kenyan Cybercriminals Siphoned Millions from America’s Sh12 Billion Student Loan System

-

Investigations5 days ago

Investigations5 days agoBetika Faces DCI Probe, Directors Arrest and License Revocation Over Massive 29.5 Million Safaricom Customers’ Data Breach

-

News1 week ago

News1 week agoEight Students Arrested In Kenya After Suspected Deadly School Arson Attack

-

News6 days ago

News6 days agoHow Uhuru’s Deal With Obama In 2015 Paved Way For America’s Ebola Plan In Kenya

-

Investigations2 weeks ago

Investigations2 weeks agoLSK On The Spot For Renewing Rogue Lawyer Dennis Onyango’s Licence Despite Mounting Evidence He Held Foreign Investors’ Millions Hostage

-

Investigations1 day ago

Investigations1 day agoCement, Cash and Courts: How the Hashu Dynasty Crushed the Ramji Brothers for Fourteen Years and Why the Walls Are Now Closing In