Business

Paybill 585555: How Airtel Kenya’s Interoperability Gateway Became A Criminal Pipeline Draining Millions From Unsuspecting M-Pesa Users

A six-digit Safaricom Paybill number linked to Airtel Money’s cross-network transfer architecture has been weaponised in a surge of unauthorised M-PESA deductions, victims reporting thousands of shillings vanishing without confirmation messages, without consent, and without recourse — exposing the catastrophic security blind spot sitting at the heart of Kenya’s celebrated mobile money interoperability system.

The number 585555 is, on paper, a legitimate piece of Kenya’s mobile money architecture. Officially registered as the Customer-to-Business Paybill number for off-net Airtel Money deposits, it was introduced as a central artery in the much-celebrated mobile money interoperability project jointly launched by Safaricom, Airtel Kenya, and Telkom in 2022 a system championed by both the Communications Authority of Kenya and the Central Bank of Kenya as the culmination of years of regulatory pressure to open up the country’s digital payments ecosystem.

The idea was elegant: any M-PESA user wanting to transfer funds directly into an Airtel Money wallet could simply dial *334#, navigate to Send Money, and route the transaction through 585555. Clean. Convenient. And, as hundreds of Kenyans are now discovering to their horror, catastrophically insecure.

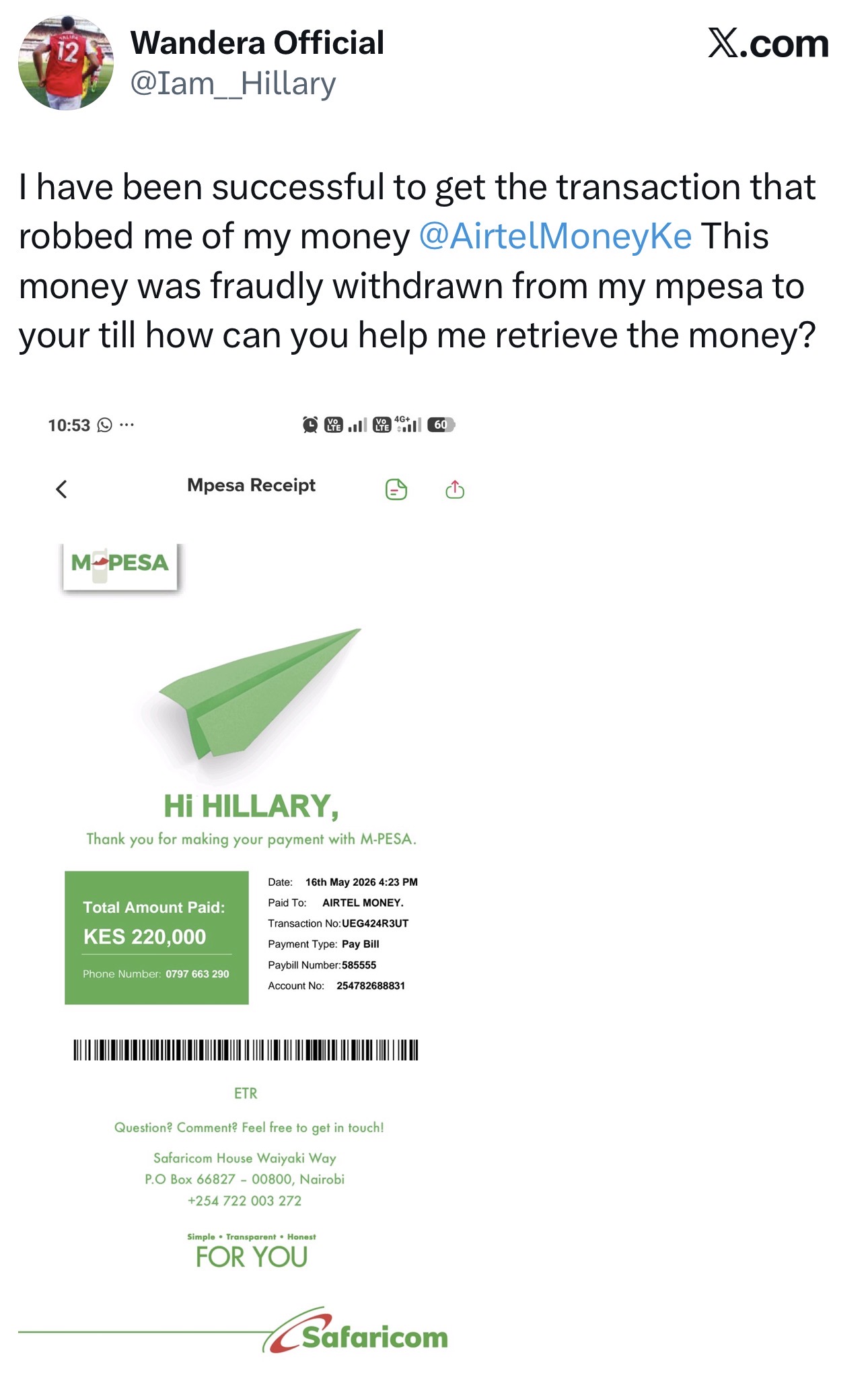

This weekend, social media platforms — in particular X, formerly Twitter — erupted with a wave of distress posts from Kenyan users who discovered money haemorrhaging from their M-PESA accounts into Paybill 585555 without their knowledge, without their authorisation, and in many documented instances, without any confirming SMS notification from Safaricom.

Transaction IDs are being shared openly, among them PFN9GVK7FP, linked to a KSh 20,700 deduction that one user discovered only after a routine balance check.

A viral post that has been shared thousands of times captured the panic spreading through Kenyan social media: “kuna mambo kwa iyo paybill 585555” — there is something wrong with that Paybill 585555. The phrase has become a watchword for a growing scandal that cuts to the heart of how Kenya’s mobile money giants have built interoperability for convenience while apparently leaving security as an afterthought.

THE ARCHITECTURE OF EXPLOITATION

To understand the full scale of the vulnerability, one must understand how Paybill 585555 actually functions within the interoperability framework.

When a Safaricom subscriber uses the *334# USSD menu to send money to an Airtel Money number, the transaction is routed via Safaricom’s network as an off-net C2B transfer a Customer-to-Business payment to 585555, which is Airtel Money’s central receiving gateway.

The account number field in the transaction captures the destination Airtel mobile number.

In properly executed, consensual transfers, the M-PESA statement reads: “Offnet C2B Transfer to 585555 — AIRTEL MONEY for Mobile No. XXXXXXX.”

Screenshot

The system was never designed to be a fraud vector.

But its architecture contains a critical structural weakness that criminal networks have learned to exploit with devastating efficiency: the Paybill gateway is publicly known, its routing logic is predictable, and once funds land in an Airtel Money wallet via this channel, cashing out is a matter of visiting any one of Airtel’s approximately 150,000 agents scattered across Kenya.

Funds transferred cross-network are extremely difficult to reverse.

As Safaricom’s own interoperability documentation makes plain, customers who experience erroneous or fraudulent transfers to 585555 cannot simply forward the transaction to 456 the standard M-PESA reversal short code.

They must contact Airtel Kenya directly, introducing bureaucratic friction that fraudsters rely upon to complete their cash-outs before any intervention is possible.

“Customers experiencing erroneous or fraudulent transfers to 585555 cannot simply use the standard M-PESA reversal channel. They must contact Airtel directly bureaucratic friction that fraudsters exploit to complete cash-outs before intervention.”

A CARRIER WITH A FRAUD HISTORY IT HAS NEVER FULLY RECKONED WITH

What makes the 585555 scandal particularly damning for Airtel Kenya is that it lands against a backdrop of documented, serial institutional failure in fraud prevention that the company has never adequately addressed before the public.

In 2018, Airtel Africa’s own prospectus filed ahead of its London Stock Exchange listing disclosed that Airtel Money operations in Kenya had suffered internally orchestrated fraud by employees that resulted in losses of 6.7 million US dollars, equivalent to approximately KSh 670 million at the time.

Only KSh 86 million was recovered through insurance. The company characterised the loss as the result of employees “circumventing controls” a clinical description for what was, in practice, a systemic collapse of internal oversight inside one of Kenya’s largest mobile money operations.

That disclosure, buried in a capital markets document, received far less regulatory scrutiny than it deserved.

And crucially, neither Airtel Kenya nor the Communications Authority conducted a public reckoning with the cultural and operational failures that produced a fraud of that magnitude.

The current 585555 controversy raises the unavoidable question: did anything actually change? The answer, based on the evidence before Kenyans this weekend, is: not enough.

THE COMESA INVESTIGATION AIRTEL HOPED YOU’D FORGET

The 585555 crisis also arrives with Airtel Money still under active scrutiny by the COMESA Competition Commission, which launched a formal investigation in February 2025 into alleged misleading practices in Airtel’s international money transfer services across Kenya, Uganda, and Malawi.

The COMESA probe found that charges displayed to the sender before confirming a transaction were, in some instances, different from the actual charges indicated in the final confirmation message. Details of intermediary parties and the exchange rates applied were allegedly not disclosed to customers.

In Uganda, customers reported receiving confirmation messages with fees that diverged materially from pre-transaction disclosures. In Malawi, charges were not disclosed at all.

Airtel Kenya’s response to that investigation was silence.

The company said it could not immediately respond to requests for comment when the probe was first announced, and has not subsequently issued any substantive public statement on the commission’s findings.

That silence has now extended to the 585555 crisis.

As of publication, Airtel Kenya has not issued any comprehensive public statement on the reported wave of unauthorised deductions. A company that cannot bring itself to respond to a regional competition commission’s transparency allegations is, it seems, equally unwilling to acknowledge when thousands of its own customers and rival network users are publicly documenting financial losses on social media.

“Airtel Kenya has not issued any comprehensive public statement on the 585555 crisis. A company silent in the face of a COMESA investigation is, it seems, equally silent when thousands document financial losses on social media.”

KENYA’S MOBILE MONEY SECURITY CRISIS: THE NUMBERS ARE TERRIFYING

The 585555 episode does not exist in isolation.

It is the latest eruption in a mobile money fraud crisis that Kenya’s regulators have been watching grow for years while doing too little to arrest it.

Between July and September 2025, the Communications Authority of Kenya’s National KE-CIRT/CC recorded 842 million cyber threat events in a single quarter. In the same period, Kenya lost an estimated KSh 29.9 billion approximately US$230 million to cybercrime.

Mobile banking fraud cases surged 87 percent in the most recent comparative reporting period, driven overwhelmingly by SIM-swap schemes, credential theft, and social engineering attacks.

A FinAccess 2024 Survey established that 9.8 percent of mobile money users in Kenya have experienced direct financial loss through fraud a rate significantly higher than those experienced through conventional banking channels.

SIM swap fraud, in particular, provides the probable mechanism behind many of the 585555 deductions reported this weekend.

A successful SIM swap gives the fraudster full control of the victim’s registered Safaricom number. With that control, the attacker can initiate M-PESA transactions, receive OTPs, and confirm transfers all while the legitimate account holder is locked out of their own number and receives no notification because the confirmation SMS is being delivered to the cloned SIM.

By the time the victim discovers the loss, the money has been received in an Airtel Money wallet via 585555 and withdrawn through one of Airtel’s agent outlets.

The money is gone.

The trail, if it exists at all, requires cooperation between two competing telecoms, the police cybercrime unit, and regulators who have historically moved at institutional speeds entirely incompatible with the velocity of mobile money fraud.

Safaricom itself is not innocent in this landscape. The company fired 113 employees for fraud-related violations in 2024.

A separately documented scheme involving 123,000 fraudulently registered SIM cards siphoned KSh 500 million through the Fuliza overdraft service. SIM swap fraud investigations at Safaricom exploded 327 percent to 47 cases in 2025.

A company that processes nearly KSh 50 billion in transactions annually and handles 28,000 SIM swap requests per day is not, evidently, building security infrastructure commensurate with the systemic risk it creates.

THE SILENCE OF THE NETWORK OWNER

What is most remarkable and most damning about the 585555 scandal is not simply that it is happening. Mobile money fraud in Kenya is not new.

What is remarkable is the institutional silence.

Airtel Kenya, whose Paybill number is the destination of these allegedly unauthorised funds, has not explained what oversight mechanisms, if any, exist on its end to detect anomalous inflows to 585555. There is no public audit mechanism.

There is no published threshold for transaction volume or velocity that would trigger a fraud alert.

There is no documented response protocol for what Airtel Money does when a cluster of transfers to its central interoperability gateway displays patterns consistent with mass fraud.

By March 2025, Airtel Money Managing Director Anne Kinuthia-Otieno was publicly celebrating the company’s full interoperability rollout and its growing market share

which had climbed from 2.9 percent to 10.3 percent by September 2025, crossing double digits for the first time in the company’s history as a percentage of Kenya’s mobile money market.

In the same period, the company was adding agents, partnering with Naivas supermarkets to extend its cash-out network, and aggressively undercutting M-PESA on fees. Growth strategy.

Expansion narrative. Security investment: absent from the press releases.

THE REVERSAL PROBLEM THAT AMOUNTS TO INSTITUTIONAL ABANDONMENT

When an M-PESA user discovers an unauthorised transfer to 585555, they enter what consumer rights advocates have described as a bureaucratic nightmare dressed up as a support system.

Standard M-PESA reversals forwarding the offending transaction to 456 do not work for cross-network transfers.

The victim must call Airtel Kenya on 0733 100 000, file a formal complaint, and then wait while Airtel Money conducts what the company euphemistically terms an investigation.

There is no statutory timeframe.

There is no guaranteed reversal.

There is no legal obligation on Airtel to refund losses arising from fraudulent use of its gateway if the fraud originated on the Safaricom side of the transaction.

A case documented in mid-2025 involving a Kenyan whose KSh 32,300 was erroneously routed to a DRC account through Airtel’s international transfer system took three weeks and the intervention of a formal regulatory complaint to the COMESA competition body before the funds were returned.

That was an error not even deliberate fraud.

The prognosis for victims of 585555-related crime, in the absence of any formal inter-carrier fraud resolution mechanism, is considerably bleaker.

The Central Bank of Kenya has acknowledged this problem.

Its National Financial Inclusion Strategy 2025-2028 contains provisions for a formal digital fraud compensation framework, theoretically targeting rollout in 2026.

Theoretically. It has not yet been implemented. In the meantime, Kenyans who have lost KSh 20,000 to fraudsters exploiting 585555 have no formal redress pathway and no legal guarantee of recovery.

“A case of KSh 32,300 erroneously routed through Airtel took three weeks and a formal regulatory complaint before the money came back. That was an error — not even deliberate fraud. The prognosis for 585555 fraud victims is considerably bleaker.”

WHAT THE REGULATORS MUST NOW ANSWER

The Communications Authority of Kenya and the Central Bank of Kenya have both received the evidence.

The 585555 complaints are not anonymous whispers they are public, timestamped, transaction-referenced posts on a major social media platform, some of them with specific M-PESA transaction IDs attached.

The question is no longer whether this fraud is happening. The question is what the regulators intend to do about it.

Kenya Insights calls on the Communications Authority to immediately convene a joint audit between Safaricom and Airtel Kenya of all transactions through Paybill 585555 over the preceding ninety days, with specific attention to velocity anomalies, timing clusters, and the geographic concentration of cash-outs on the Airtel Money side.

The Central Bank must activate its Consumer Protection Framework and require Airtel Kenya to publish, within 30 days, a full account of the fraud detection and monitoring protocols it has deployed on its interoperability gateway.

The National Police Service cybercrime unit must initiate a formal criminal investigation into the specific transaction IDs being reported by victims online.

And Safaricom must acknowledge publicly that the security architecture of its *334# interoperability pathway contains vulnerabilities that are being actively exploited.

The High Court’s March 2026 ruling banning arbitrary phone number recycling by telecoms following a petition that argued a phone number had become, in effect, a digital identity encompassing M-PESA, banking OTPs, KRA PIN access, and email recovery is directly relevant here.

If courts have recognised that a phone number is a citizen’s digital identity, then the exploitation of mobile money gateways through SIM compromise is, functionally, identity theft at scale.

It must be treated and prosecuted accordingly.

A COMPANY GROWING ITS MARKET SHARE WHILE LEAVING ITS CUSTOMERS EXPOSED

Airtel Kenya has spent the last three years building a compelling challenger narrative.

It has undercut M-PESA on fees.

It has expanded its agent network to 150,000 outlets. It has crossed 11 percent market share. It has celebrated two million Airtel Money Paybill merchants.

All of this is genuine commercial achievement. But a mobile money operator that grows its market share by acquiring custodianship of an increasing percentage of Kenyan citizens’ digital financial lives takes on a corresponding and proportionate responsibility for the security of those lives.

Airtel Kenya has, on the evidence before Kenya Insights, not discharged that responsibility.

The company that disclosed a KSh 670 million internal fraud in 2018 without a public reckoning, that faces a COMESA investigation into deceptive charging practices in 2025 without a public response, and that now operates the interoperability gateway at the centre of a mass fraud complaint without a public statement has forfeited the right to continue expanding its digital payments infrastructure without direct, structured regulatory oversight of its security protocols.

Airtel Africa’s Nairobi operation must open its books to the Communications Authority.

Its 585555 gateway transaction logs must be turned over to investigators. Its senior management must appear before the relevant parliamentary committee.

And if the evidence establishes that Airtel Money has been receiving fraudulently generated transfers into its gateway while its fraud monitoring was absent, inadequate, or deliberately suppressed, the company must face the full weight of Kenya’s computer fraud statutes.

Kenya built the world’s most innovative mobile money system. The world watched, admired, and copied it. The country deserved then, and deserves now, telecoms that protect what they built.

Paybill 585555 is not just a fraud number. It is a referendum on whether Airtel Kenya is fit to hold the trust of the Kenyan people.

Kenya Insights allows guest blogging, if you want to be published on Kenya’s most authoritative and accurate blog, have an expose, news TIPS, story angles, human interest stories, drop us an email on [email protected] or via Telegram

Why Ruto’s Favourite Candidate Adan Mohammed Could Be Locked Out of the KRA Top Job

DCI Arrests Woman in Sh55.7 Million Gold Fraud Targeting American Citizen in Nairobi

Court Confirms Safaricom Customers Data Was Sold To Betting Companies In Seven-Year Cover-Up

Paybill 585555: How Airtel Kenya’s Interoperability Gateway Became A Criminal Pipeline Draining Millions From Unsuspecting M-Pesa Users

The Man Who Starved Kenya’s Voice

The Rot Inside Absa: How Bank Insiders Are Looting Nairobi’s Customers

The President’s Helicopter: How Ruto’s Aviation Empire Lands a Historic Airbus Milestone While His Government Writes the Tax Code

“TikTok Who? YouTube Sorry. A Kenyan-Built Platform Just Dropped—and 20 African Ministers Showed Up To Launch It.”

Denial Under Duress: The Untold Collapse Threatening David Lagat’s DL Group’s Empire

Stung By West Africa Rejections, France Courts Rest Of Continent at Kenya Summit

How Did a Sh468K KRA Salary Allegedly Turn Into Sh30 Billion? Questions Deepen Over Commissioner George Obel and Ciala Resort Owner’s Wealth

Nairobi Freezes Binance Accounts in Sweeping Anti-Fraud Crackdown as Global Scandal Record Haunts World’s Largest Crypto Exchange

THE UNTOUCHABLE CLERK: How Fatuma Mwalupa Allegedly Turned Kwale Assembly Into a Personal Treasury and Outsmarted Scrutiny

The Man Behind the Badge: How Prof. Erastus Kanga Turned Kenya’s Premier Wildlife Agency into a Theatre of Corruption, Fear and Impunity

THE BRAZEN RETURN: Triton Thief Yagnesh Devani, Who Pillaged Kenya of Sh7.6 Billion and Fled, Now Asks the Same Courts He Escaped to Restore His Stolen Wealth

Green Gold, Rotten Roots: How Kenya’s Biggest Avocado Firms Hijacked a Sh5.8 Billion Harvest Ban

Why the April 21 Flopped Protests Expose Kenya’s Rudderless Opposition

KETRACO CEO Advert Marred By Controversies As Fears Grow That Kipkemoi Kibias Is A Predetermined Candidate

THE PHANTOM COVER: Unlicensed Broker Vanishes With Sh42M, Hussein Mohammed Fingered In The Alleged CHAN 2024 Insurance Scandal

64-Year-Old KIM Faces Shutdown As Regulator Declares Its Certificates Worthless, Orders Employers To Shun Graduates

-

Business1 week ago

Business1 week agoSafaricom’s Sh1.4 Billion Reckoning: How Kenya’s Most Profitable Company Stole a Man’s Idea and Got Caught

-

Africa2 weeks ago

Africa2 weeks agoThe $24 Million Heist at the End of the World

-

Business1 week ago

Business1 week agoTHE INSURER THAT TOOK YOUR PREMIUM AND FORGOT YOUR NAME: How ICEA Lion Left a Client Begging for Sh7.8 Million Across Four Months

-

Investigations1 week ago

Investigations1 week agoDenial Under Duress: The Untold Collapse Threatening David Lagat’s DL Group’s Empire

-

Business4 days ago

Business4 days agoThe Rot Inside Absa: How Bank Insiders Are Looting Nairobi’s Customers

-

Business1 week ago

Business1 week agoBush Air Safaris Founder John Ndiritu Risks Losing Property Over Disputed Loan Claim

-

Arts & Culture2 weeks ago

Arts & Culture2 weeks agoKDC Accelerates the Creative Economy, Innovation and Youth-Led Enterprise Growth at Africa Forward Summit

-

Africa1 week ago

Africa1 week agoStung By West Africa Rejections, France Courts Rest Of Continent at Kenya Summit