Business

THE EMPIRE FIGHTS BACK: How Safaricom’s War on Starlink Shapes Kenya’s Satellite Future

As the Communications Authority reviews Airtel’s landmark direct-to-cell application, the Kenyan telecom market is gripped by a battle that is simultaneously commercial, regulatory and deeply political. At its centre: a dominant incumbent, a satellite disruptor, and a state that wants visibility over every byte of data its citizens send.

When the Communications Authority of Kenya quietly confirmed that it has opened a formal review of Airtel Kenya’s application to introduce Starlink’s direct-to-cell satellite service, the announcement arrived with the understated tone of routine regulatory administration. It was anything but.

Beneath the procedural language of frequency coordination and interference thresholds sits one of the most consequential contests in Kenya’s telecoms history: who controls the invisible architecture of digital connectivity, and on whose terms does the next generation of internet access get built.

The answers to those questions are being written right now, in meetings between regulator and operator, in the corridors of Parliament, and in the strategic rooms of a company that has spent decades turning market dominance into institutional permanence.

“The satellites act as cell towers in space. Any 4G smartphone can connect. No extra hardware. No fibre contract. No incumbent.” That is the proposition Safaricom spent 2024 trying to bury.

Airtel Africa announced in December 2025 that it had signed a partnership with SpaceX to roll out Starlink’s Direct-to-Cell technology across all 14 of its African markets beginning 2026.

The service works by equipping satellites in low Earth orbit with evolved Node B modems, the same radio equipment used in conventional 4G towers, enabling standard smartphones to connect directly to satellites when terrestrial coverage is unavailable. No satellite dish. No specialised device. Just a sky view and a compatible handset.

The initial rollout covers text messaging and basic data for select applications, with voice capability and broadband-grade speeds on a roadmap through 2028.

The CA confirmed to the media that it has received a formal application from Airtel Networks Kenya Limited and that discussions are ongoing.

The regulator says its primary technical concern is the potential for harmful interference: transmissions from higher-power low Earth orbit satellites can degrade noise levels in the licensed spectrum bands used by ground-based 3G, 4G and 5G networks. It is a legitimate engineering problem.

It is also the kind of argument that has, in the Kenyan market, a habit of being deployed as cover for competitive resistance.

THE LETTER THAT STARTED IT ALL

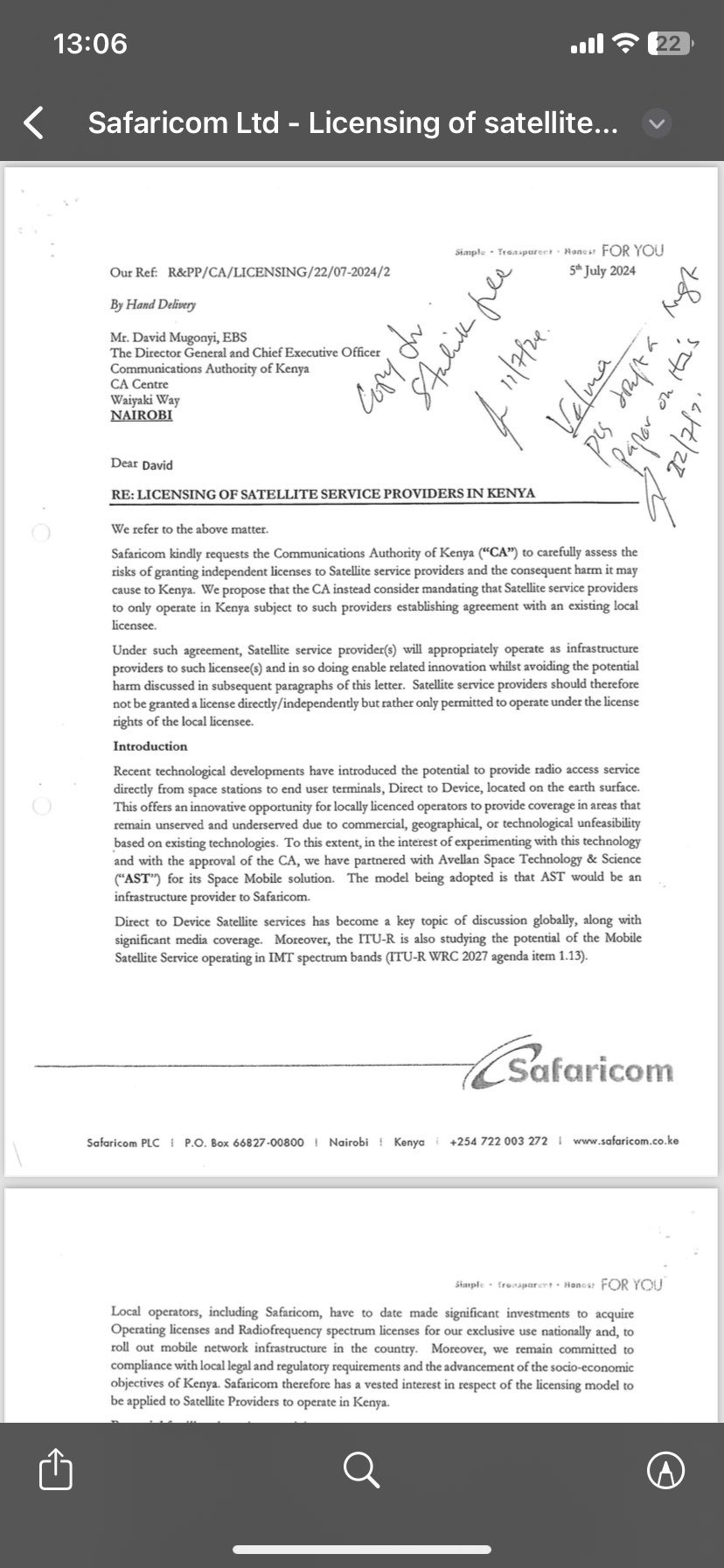

Rewind to July 2024. Safaricom’s director for broadband services, Tom Waithaka, put his name to a formal submission to the CA that, had it succeeded, would have fundamentally altered Starlink’s position in Kenya.

The letter, later leaked and reported by multiple outlets including this publication, argued that satellite coverage inherently extends across territorial borders and, in the absence of effective management, could provide services illegally and cause harmful interference to mobile networks. Safaricom’s prescription was precise: satellite internet providers should not be granted independent operating licences. They should instead be classified as infrastructure providers, permitted only to operate through partnerships with existing local licensees.

The argument was dressed in regulatory language, but its commercial logic was transparent. Starlink had entered the Kenyan market in July 2023 and had immediately disrupted the pricing structure that local operators, Safaricom chief among them, had spent years calibrating.

The entry price for a Starlink kit was initially steep at Sh89,000, but the American firm moved aggressively, slashing terminal costs to Sh45,500 and introducing monthly rental options at Sh1,950, making it genuinely accessible to a swelling middle class that had grown restless with the quality and cost of terrestrial broadband.

Monthly data packages entered the market as low as Sh1,300, a figure that put competitive pressure on the entire local ISP sector.

The CA, to its credit, held its ground. It told the court handling a parallel challenge brought by rights group Kituo Cha Sheria that it viewed Safaricom’s submission as the position of a market participant with a direct commercial interest, and that it was not bound to act on it.

The regulator noted that Safaricom was, in the court’s own language, directly prejudiced by its market dominance and likely apprehensive about the entry of new players.

That was then. In August 2024, Safaricom’s subscriber-growth machine was still running at pace. Its market share stood north of 65 percent. M-Pesa was the unrivalled architecture of Kenyan mobile money. The company could afford to fight.

THE EROSION BEGINS

Eighteen months later, the numbers tell a different story. Safaricom’s mobile subscriber market share has slid in consecutive quarters, falling from 65.7 percent in September 2024 to 64.4 percent by the end of 2024 and further to 63.3 percent in the first quarter of 2025.

In the same period, Airtel Kenya added nearly three million new subscribers, lifting its share to a record 32.2 percent.

Airtel Money, the company’s mobile wallet, punched through to double-digit market share for the first time, squeezing an M-Pesa platform that has now spent six consecutive quarters losing ground, even as it still commands around 90 percent of the mobile money market.

The competitive strain does not end at subscriber numbers. In March 2026, the CA implemented a further reduction in mobile termination rates, cutting the interconnection fee that operators charge each other for completing calls from Sh0.41 to Sh0.37 per minute.

The revision is the latest in a series of phased reductions that have compressed an income stream Safaricom has historically relied upon.

In the year ending March 2025, the company collected Sh4.7 billion in interconnection revenue, down from Sh5 billion the year before, itself a decline from the higher figures that prevailed before prior regulatory reviews.

Safaricom is the net beneficiary of termination fees precisely because it is the largest network: when the regulator trims the rate, the biggest network absorbs the largest absolute loss.

The company has been open about its anxiety. In its most recent regulatory filings, Safaricom listed market disruption and competition among its top ten strategic risks, a disclosure that would have been unthinkable five years ago for a company that then appeared structurally immune to challenge.

Its response to the competitive pressure has been partly technical, partly reactive. In September 2024, weeks after the Starlink-driven pricing panic, Safaricom quietly upgraded speeds on its home fibre packages to stem subscriber flight. It worked temporarily. But the structural arithmetic has not changed.

Mobile data revenue has now overtaken voice revenue for the first time in Safaricom’s history, reaching Sh44.4 billion in the half-year to September 2025, an 18 percent increase.

That figure looks impressive until one considers that data pricing is under perpetual downward pressure from Airtel, which charges less for comparable bundles, and from Starlink, which is redefining what affordable broadband looks like in areas beyond the fibre grid.

A Direct-to-Cell service that brings satellite broadband to any standard smartphone, without infrastructure investment by the subscriber, threatens the one revenue pool that Safaricom has successfully grown while voice and interconnection decline.

Data is now Safaricom’s beating heart. A space-based competitor that can reach every corner of Kenya without a single fibre cable is not a nuisance. It is an existential variable.

THE ARCHITECTURE OF CAPTURE

Safaricom’s July 2024 letter was not the company’s first attempt to shape the competitive environment through regulatory channels rather than product competition.

The company has a documented history of engaging regulators, courts and government when new entrants threaten its ecosystem. It opposed the attempted merger of Airtel Kenya and Telkom Kenya on grounds of spectrum rebalancing and debt obligations. When Starlink introduced rental options and slashed kit prices in mid-2024, Safaricom’s submission to the CA arrived within weeks.

What makes the Starlink episode distinctive is that it activated the entire weight of the regulatory apparatus simultaneously.

Starlink.

The CA turned to the International Telecommunication Union for a global framework rather than applying existing Kenyan rules, effectively delaying a definitive regulatory posture.

A court case brought by Kituo Cha Sheria to defend Starlink’s independent operation was met with the CA arguing that the NGO’s suit was a proxy for Starlink’s commercial interests. The government, meanwhile, was simultaneously pursuing a registration and identity verification drive targeting Starlink subscribers specifically.

That verification requirement, announced in February 2026 under the Kenya Information and Communications (Registration of Telecommunications Service Subscribers) Regulations 2025, mandates that all Starlink users complete in-person identity verification at an authorised retailer by April 30, 2026, or face service interruption.

Starlink is required to collect national identity cards, postal addresses and phone numbers of each subscriber and authenticate them against the National Integrated Population Registration System. The consequence of non-compliance is deactivation.

The CA frames the requirement as routine extension of Kenya’s Know Your Customer framework to satellite services. The language of security and fraud prevention runs through every official statement on the matter.

But the practical effect is to eliminate one of the structural advantages that had made Starlink attractive to a specific and significant segment of Kenyan subscribers: those who had, after the events of 2024, become acutely conscious of what their digital footprint meant.

THE SURVEILLANCE DIMENSION

The year 2024 was, for Kenya, a year of rupture. Gen Z-led protests against the Finance Bill brought hundreds of thousands onto the streets in June and July, producing one of the most consequential political upheavals of the Ruto administration.

The government’s response involved police live fire that killed dozens.

It also, according to investigations by the Daily Nation, Nairobi-based journalist Namir Shabibi and international outlet The Continent, involved the systematic use of subscriber data by security agencies.

The investigation, published in October 2024, alleged that Safaricom had allowed security agencies routine access to call data records and location data without court orders, assisting in the tracking and capture of individuals linked to the protest movement.

The Kenya Human Rights Commission and Muslims for Human Rights wrote a formal open letter to Safaricom CEO Peter Ndegwa detailing specific allegations: that the company had facilitated the handling of call data records by police attached to its own Law Enforcement Liaison Office, creating a conflict of interest in which the accused agency controlled access to evidence of its own conduct; that it had produced records bearing signs of manipulation before courts; that it had retained data it claimed had been deleted; and that it had, in partnership with Neural Technologies Limited, developed a software system granting security agencies what the rights groups described as virtually unfettered access to subscriber data.

The Kenya National Commission on Human Rights documented more than 80 cases of abductions and enforced disappearances following the protests.

Activists who had been targeted publicly said they had abandoned their Safaricom lines in an effort to evade tracking, encouraging others to do the same. US Ambassador Meg Whitman weighed in, describing the mobile phone surveillance by security agents as a breach of privacy.

Safaricom denied the allegations categorically.

CEO Ndegwa said during the company’s half-year results presentation that the reports were inaccurate and that sharing subscriber data without a court order would produce chaos in the business.

The company noted its ISO 27701 certification from the British Standards Institute for privacy information management. Its lawyers filed a complaint against Nation Media Group with the Media Council Complaints Commission, alleging that the publication had violated the journalism code of conduct.

Safaricom CEO Peter Ndegwa.

The Senate launched an ICT committee probe. Senators demanded to know whether Safaricom had a data-sharing agreement with the government and whether subscribers had been informed. The answers were never definitively provided.

What the episode established, beyond reasonable dispute, is that Kenyan security agencies regard telco subscriber data as an operational asset, that the legal framework governing access to that data is porous and contested, and that the established operators, whether by design or systemic pressure, have operated within a surveillance ecosystem that serves state objectives.

Against that backdrop, Starlink’s architecture represented something genuinely disruptive that had nothing to do with data speeds or pricing.

A satellite operator headquartered in the United States, routing traffic through a constellation in low Earth orbit, does not sit inside the reach of the Law Enforcement Liaison Office.

Accessing subscriber data from Starlink requires going through Starlink, which means navigating American corporate governance, US federal law and SpaceX’s own policy frameworks. For anyone who had spent 2024 watching their compatriots disappear after their calls were traced, that was not an abstract distinction.

Joseph Khago, a Nairobi-based IT specialist, framed the implications of the KYC mandate with characteristic directness when speaking to this publication.

Without the registration requirement, he noted, authorities seeking to identify a Starlink user from an IP address would have to go through the company itself. The new regulations give the government more control.

What he did not need to add is that they simultaneously diminish one of the most significant practical privacy advantages that satellite broadband had offered to ordinary Kenyan internet users.

Starlink’s architecture bypassed the surveillance architecture that terrestrial operators had spent a decade building with, and sometimes for, the Kenyan state. The KYC mandate closes that gap.

PEACE IN OUR TIME

Safaricom’s formal posture toward Starlink changed with conspicuous speed once the competitive arithmetic shifted. By late September 2024, CEO Ndegwa was telling interviewers that the company was open to discussions with satellite providers and viewed their technology as complementary.

In November 2025, Safaricom’s parent company Vodacom signed a continent-wide agreement with SpaceX authorising Vodacom and its subsidiaries, including Safaricom, to resell Starlink’s satellite internet equipment and services to enterprise and small business customers across Africa.

The deal was announced as a strategic evolution. In operational terms it is more accurately described as absorption: Safaricom gains a distribution relationship with the disruptor, integrating satellite backhaul into its network to reach remote areas without the capital cost of new towers, while Starlink gains a distribution partner with 50 million subscribers and a retail infrastructure that extends to the furthest reaches of the country.

Both sides benefit. But the dynamic is not symmetrical. Safaricom retains control of the customer relationship, the billing relationship and the data relationship. Starlink enters as a supplier.

The Airtel deal is structurally different, and that difference explains everything.

Where Safaricom’s Starlink integration uses satellites to relay data between remote towers and the core network, the Direct-to-Cell arrangement turns the satellite into the tower. The customer connects directly to the sky.

There is no Airtel-controlled data path in a dead zone; the connection is established between handset and satellite, with Airtel providing the licensed LTE spectrum that makes the integration legal.

This is the architecture that Safaricom’s 2024 letter was specifically designed to prevent. It is the model that was, in the language of that letter, too risky to license independently.

Airtel, of course, is not Starlink operating independently. It is a licensed Kenyan mobile operator using licensed Kenyan spectrum to partner with a satellite provider.

That is precisely the model Safaricom claimed to want: satellite as infrastructure, working through a local operator.

The irony is that the local operator enabling it is Safaricom’s most aggressive competitor. Airtel Kenya CEO Ashish Malhotra has not been coy about the strategic ambition.

The promise that every Airtel customer in every corner of Kenya will get coverage the day approval comes is not just a connectivity statement. It is a competitive declaration addressed to a market leader whose rural reach has been one of its most durable advantages.

THE REGULATOR’S TIGHTROPE

The CA’s position in this contest is genuinely difficult, and there is reason to believe that the current review reflects something more than procedural caution. The interference concern is real: the GSMA, the ITU and independent telecoms analysts have all noted that high-power LEO satellite transmissions in flexible-use spectrum bands can degrade noise floors in ground networks. The CA will need to model signal propagation, assess the satellite constellation’s orbital parameters and determine operational conditions that protect existing licensees. That work takes time and requires technical capacity.

What complicates the picture is that the CA’s track record on Starlink regulation has shown a consistent tendency to move slowly in ways that favour incumbents.

The ITU referral in 2024 was cited by some industry observers as a means of deferring a decision that would otherwise have required the regulator to either grant or deny Starlink’s operating model explicitly.

Safaricom is itself a partial government asset, with the Kenyan state holding a stake through the National Treasury alongside Vodacom and Vodafone. The institutional relationships that flow from that ownership structure do not require conspiracy to function as competitive cushioning.

Airtel Kenya has a record of filing competition complaints against Safaricom over regulatory processes.

In the LTE licensing process of the mid-2010s, Airtel and Telkom Kenya both raised objections about the manner in which the 4G licence was awarded to Safaricom. That grievance was never resolved in a manner satisfactory to the smaller operators. The frequency rebalancing dispute that Safaricom cited in opposing the Airtel-Telkom merger was, in the view of Airtel’s lawyers, precisely the kind of regulatory asymmetry that entrenches dominance under the cover of technical administration.

The CA has, under the current government, moved to address at least one dimension of competitive imbalance.

The reduction in mobile termination rates, opposed strenuously by Safaricom and implemented over its objections, is a structural intervention designed to reduce the automatic income advantage that accrues to the largest network.

The logic of the Airtel-Starlink review should, in principle, run along similar lines: a technology that demonstrably extends coverage into underserved areas, using a licensed operator and licensed spectrum, should face a clear regulatory path.

Whether it will is the question that the market, and Safaricom’s board, is watching with intense interest.

WHAT A DECISION WOULD MEAN

The CA’s approval of the Airtel-Starlink Direct-to-Cell service would reshape the competitive landscape in ways that cannot be contained by Safaricom’s current countermeasures.

The technology does not require terrestrial infrastructure in the areas it covers. It reduces the capital cost of extending coverage to rural and pastoral regions, which have been the most durable source of Safaricom’s network advantage.

An Airtel customer in a dead zone who can send a text, access emergency services or use a data application directly via satellite is no longer captive to whoever owns the nearest tower.

The data pricing implications are potentially more significant still. Direct-to-Cell is initially limited in bandwidth capacity per satellite, but the roadmap that Airtel and SpaceX have publicly committed to includes next-generation satellites with data speeds described as twenty times greater than the first generation.

If that roadmap executes on schedule, the service moves from a coverage solution for dead zones to a competitive broadband product for anyone with sky visibility.

In a country where Safaricom’s mobile data revenue has become the primary growth engine, a satellite-delivered alternative that bypasses the terrestrial network is not a fringe concern. It is a core revenue threat.

Starlink’s current position in Kenya’s fixed internet market, at 0.8 percent with roughly 19,470 subscribers, understates its competitive trajectory. The company grew at more than 2,500 percent between its entry and December 2024.

The KYC mandate, the CA’s regulatory pace and the absence of a Direct-to-Cell approval have collectively dampened that growth. Remove those constraints and the growth dynamics change. Add a distribution partner with Airtel’s subscriber base and agent network, and the dynamics change again, at Safaricom’s direct expense.

CONCLUSION: THE SATELLITE AND THE STATE

Kenya’s satellite internet story is not, at its core, a story about technology. It is a story about power: who holds it, who extends it, and who is threatened when the underlying architecture of connectivity shifts in ways that cannot be controlled from the top of the existing hierarchy.

Safaricom spent 2024 attempting to use the regulatory system to slow a competitor whose fundamental business model challenged the proposition that you need a tower, a cable and a licensed operator in your vicinity to get online.

It failed to stop Starlink’s entry, but it succeeded in framing the terms of Starlink’s integration into the Kenyan ecosystem in ways that preserve the data relationship between subscribers and a state that has demonstrated it regards that relationship as an operational resource.

The Airtel partnership now tests whether the CA is willing to approve a Direct-to-Cell model that, if it scales as its architects intend, materially changes the competitive landscape for the dominant operator and, as a consequence, changes the surveillance arithmetic for a state whose security agencies have shown a persistent appetite for subscriber data from within the country’s borders.

That is not a regulatory question with a clean technical answer. It is a political and commercial question dressed in the language of spectrum management.

The CA has said it is reviewing the application. The market is watching the clock.

Kenya Insights allows guest blogging, if you want to be published on Kenya’s most authoritative and accurate blog, have an expose, news TIPS, story angles, human interest stories, drop us an email on [email protected] or via Telegram

Yet Another Blow for Bia Tosha as Court Rejects Bid to Halt Diageo–Asahi Transaction

US to Slash Number of African Embassies Processing Visas from 50 to 20, Kenya Remains a Key Hub

Trump Picks Veteran Crisis Diplomat Henry Wooster as New U.S. Ambassador to Kenya

Former Catholic Priest Arrested Over Alleged Treasonous Social Media Posts

Hundreds Protest Against Planned US Ebola Quarantine Facility in Kenya

President Ruto Defends Laikipia Ebola Quarantine Centre, Tells Critics to ‘Relax’

“Raila Died Walking, He Didn’t Collapse,” Maurice Ogeta Breaks Silence On His Boss’ Final Moments

Bolt Denies Viral Exit Claims, Says Kenya Operations Remain Fully Active

Secret Trident Meetings, Claims of Millions Exchanged: Fresh Questions Raised Over PCF Boss Mohammed Sahal’s Role in Insurance Battle

The Kamukunji Cash Pit: Ghost School, Phantom Audit Trails and NG-CDF Manager Who Refuses to Leave

Why Ruto’s Favourite Candidate Adan Mohammed Could Be Locked Out of the KRA Top Job

Este Medical Kenya Fights American’s Explosive Complaints

Safaricom’s Sh1.4 Billion Reckoning: How Kenya’s Most Profitable Company Stole a Man’s Idea and Got Caught

LifeCare on the Brink: SHA Fraud, Stolen Wages, and the Rotten Empire Jayesh Saini Built

The Rot Inside Absa: How Bank Insiders Are Looting Nairobi’s Customers

The $24 Million Heist at the End of the World

Denial Under Duress: The Untold Collapse Threatening David Lagat’s DL Group’s Empire

THE INSURER THAT TOOK YOUR PREMIUM AND FORGOT YOUR NAME: How ICEA Lion Left a Client Begging for Sh7.8 Million Across Four Months

Court Confirms Safaricom Customers Data Was Sold To Betting Companies In Seven-Year Cover-Up

Eight Students Arrested In Kenya After Suspected Deadly School Arson Attack

-

News1 week ago

News1 week agoEste Medical Kenya Fights American’s Explosive Complaints

-

Investigations1 week ago

Investigations1 week agoLifeCare on the Brink: SHA Fraud, Stolen Wages, and the Rotten Empire Jayesh Saini Built

-

News4 days ago

News4 days agoEight Students Arrested In Kenya After Suspected Deadly School Arson Attack

-

Americas1 week ago

Americas1 week agoInside FAFSA Fraud: How Kenyan Cybercriminals Siphoned Millions from America’s Sh12 Billion Student Loan System

-

Business2 weeks ago

Business2 weeks agoBlocked: How Mombasa Tycoon Ashok Doshi Has Stopped Imperial Bank Depositors From Getting Their Money

-

Investigations1 week ago

Investigations1 week agoLSK On The Spot For Renewing Rogue Lawyer Dennis Onyango’s Licence Despite Mounting Evidence He Held Foreign Investors’ Millions Hostage

-

News2 days ago

News2 days agoHow Uhuru’s Deal With Obama In 2015 Paved Way For America’s Ebola Plan In Kenya

-

Investigations2 days ago

Investigations2 days agoBetika Faces DCI Probe, Directors Arrest and License Revocation Over Massive 29.5 Million Safaricom Customers’ Data Breach