Business

Sh11 Billion Zakhem Debt Bombshell Rocks Kenya Pipeline Three Months After IPO, As Questions Mount Over What Investors Were Told

Barely three months after Kenya Pipeline Company PLC made history as the first state enterprise to list on the Nairobi Securities Exchange under President William Ruto’s privatisation programme, the newly public company has been hit with a fresh lawsuit that could cost it close to eleven billion shillings, reigniting a decade old fight with a Lebanese contractor and forcing investors to confront a question they thought had already been answered before they bought their shares.

On June 15, 2026, KPC issued a cautionary announcement to shareholders disclosing that Zakhem International Construction Limited had filed suit at the Milimani High Court, case number HCCOMM E346 of 2026, seeking a combined USD 84.1 million, equivalent to roughly KSh10.89 billion.

The figure is dominated not by the original contractual dispute but by interest.

According to the breakdown contained in the announcement, Zakhem is claiming USD19,036,187.46 in extension of time costs and a staggering USD65,081,253.70 in accumulated interest on delayed payments, a ratio that tells its own story about how long this fight has been allowed to fester and how expensive Kenyan institutions have made it for themselves to stall.

KPC’s company secretary and General Manager for Legal Services, Flora Okoth, signed off on the notice, telling shareholders that the board, “based on the information currently available and the preliminary legal advice it has received from the Company’s advocates, is of the view that the Company has credible legal and factual grounds upon which to contest the claim.” The same notice carried the now familiar caution to the investing public to “exercise caution when dealing in the securities of the Company pending the resolution of the matter.”

For a company whose shares were sold to the public on the strength of its position as one of the most profitable state corporations in Kenya, a pipeline operator moving the lifeblood of the economy from Mombasa to Nairobi, the timing could hardly be worse.

A FIGHT THAT NEVER ENDED

To understand why this latest claim landed with such force, it helps to go back to 2014, when KPC awarded Zakhem a contract worth approximately USD484.5 million for the procurement, construction, testing and commissioning of the Line 1 Replacement Project, the 450 kilometre pipeline carrying refined petroleum products between Mombasa and Nairobi under contract number SU/QT/032/13.

The project, once completed, did not bring the dispute to a close. Zakhem filed suit in 2019, HCCC E322 of 2019, claiming it had not been paid sums due under the contract.

In June 2020, the High Court entered a partial summary judgment in Zakhem’s favour for USD44,019,024.64. What followed was years of argument over how that decree should be satisfied, much of it tangled up with the Kenya Revenue Authority.

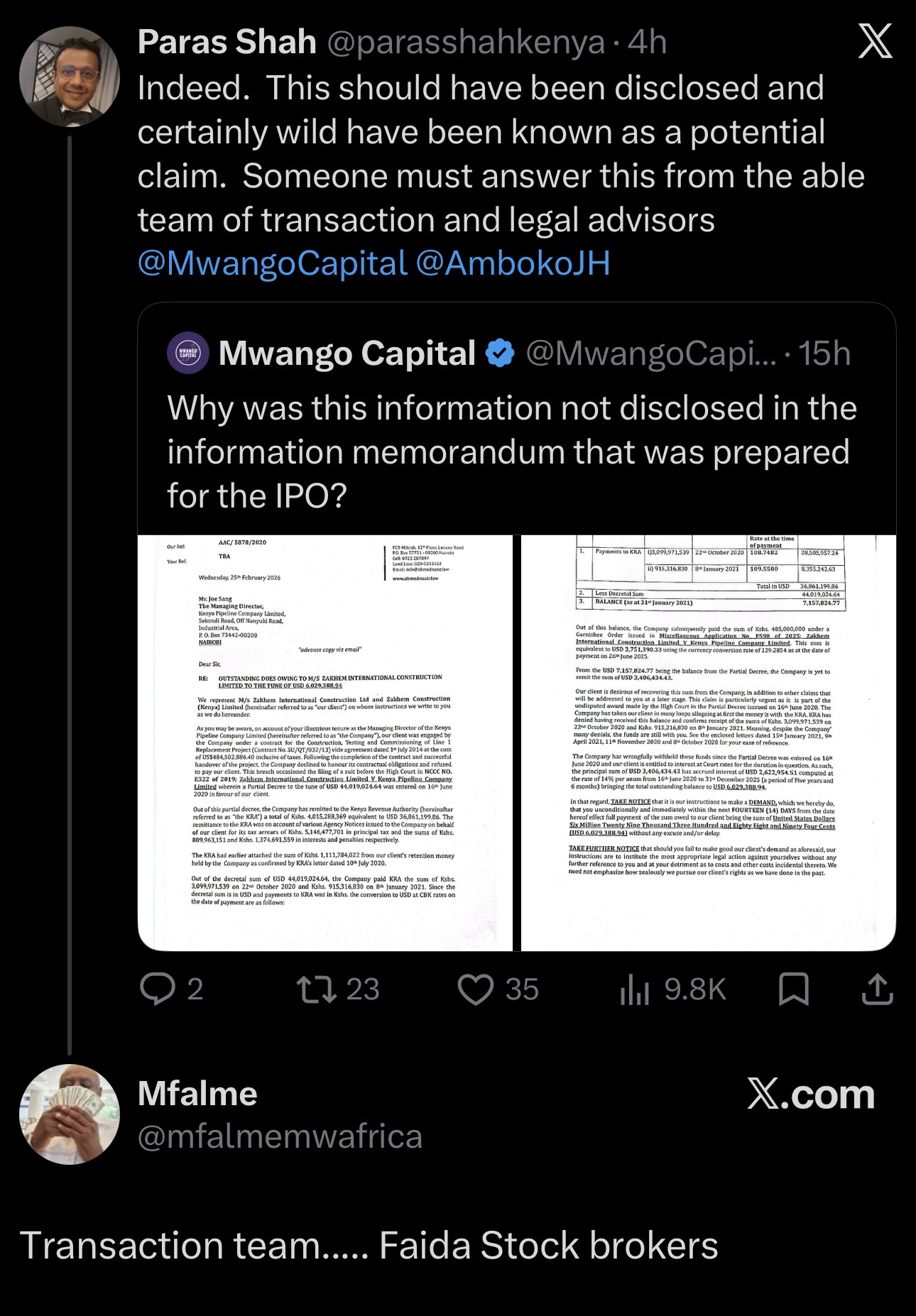

According to a demand letter dated February 25, 2026 from Ahmednasir Abdullahi Advocates LLP, acting for Zakhem, KRA had issued agency notices against KPC’s accounts for tax arrears tied to the Zakhem payments, and KPC ultimately remitted a total of USD36,861,199.86 to KRA in two tranches, KSh3.099 billion in October 2020 and KSh915.3 million in January 2021. After deducting these remittances from the decretal sum, the letter calculates a residual balance of USD7,157,824.77 as at January 31, 2021.

From that balance, Zakhem says it has so far recovered only part of what it is owed. In June 2025, the Lebanese contractor obtained a garnishee order absolute against KPC’s accounts at Equity Bank, extracting KSh485 million, equivalent to roughly USD3.75 million at the prevailing exchange rate.

That left, by Zakhem’s calculation, a principal balance of USD3,406,434.43 still outstanding from the 2020 decree, on which interest at the court rate of 14 percent per annum had by the law firm’s reckoning ballooned to USD2,622,954.51 over five and a half years, bringing that single residual claim to USD6,029,388.94. The February letter gave KPC fourteen days to pay or face further legal action, and warned explicitly that “other claims that will be addressed to you at a later stage” were still coming.

Four months later, they arrived. The USD84.1 million claim filed in June 2026 is that “later stage.” It is a new and separate action under a new case number, built around extension of time claims and a fresh interest calculation running on the broader contract, not merely the residual balance from the 2020 decree. Put simply, this is not Kenyan officialdom being blindsided by an old, forgotten file. It is the predictable next instalment of a dispute that Zakhem’s lawyers had been openly signalling for months, in writing, with deadlines attached.

WHAT INVESTORS WERE ACTUALLY TOLD

This is where the story gets complicated, and where the loudest voices on social media may be aiming their fire at the wrong target, or at least an incomplete one.

Within hours of KPC’s cautionary announcement, the question that mattered most to retail investors began circulating on X.

Mwango Capital, a widely followed markets commentary account, asked directly: “Why was this information not disclosed in the information memorandum that was prepared for the IPO?” Markets commentator Paras Shah amplified the point, arguing that the matter “should have been disclosed and certainly wild have been known as a potential claim,” and called on “the able team of transaction and legal advisors” to answer for it. Another user went further, naming Faida Investment Bank’s transaction team directly.

Screenshot

It is a fair question to ask. It is also, on the public record, not quite as simple as “this was hidden.”

KPC’s Information Memorandum, dated 17 January 2026 and prepared under the stewardship of Faida Investment Bank Limited as Lead Transaction Advisor, with TripleOKLaw Advocates LLP and G&A Advocates LLP as joint legal advisers, was not the first time Kenyans had been told that KPC was carrying contingent liabilities tied to Zakhem.

Months earlier, in October 2025, Parliament adopted Sessional Paper No. 2 of 2025, the policy document that formally approved KPC’s privatisation through an IPO.

According to reporting at the time by the Business Daily and the Kenyan Wallstreet, that sessional paper explicitly flagged that pending lawsuits would consume Sh5.75 billion of the privatisation proceeds, and itemised among those liabilities “a garnishee order of Sh485 million in favour of M/s Zakhem International following contractual disputes.”

The paper’s own policy resolutions stated that the Privatisation Commission was to ensure “all liabilities-debt and credit and risks affecting the valuation of KPC are comprehensively assessed, transparently disclosed, and factored into the transaction valuation before proceeding with the IPO.”

In other words, the Zakhem name, the Sh485 million figure, and the existence of an active, contractually rooted dispute over the Line 1 project were sitting in a parliamentary policy document months before Faida’s transaction team and the legal advisers sat down to finalise the Information Memorandum, and that document was itself covered in the mainstream business press.

What appears to be different, and what the IM critics have not yet been able to point to with documentary proof, is whether the January 2026 Information Memorandum’s risk factors and litigation sections carried forward that same level of specificity, naming Zakhem and quantifying the live exposure, including the open-ended threat contained in the February 2026 Ahmednasir Abdullahi demand letter that “other claims” would follow.

That demand letter was dated five weeks before the IPO closed and roughly three weeks after the IM itself was dated, raising a narrower but sharper question: not whether KPC’s contingent liabilities were known to exist in general terms, but whether the live, escalating, lawyer-flagged threat of a fresh multi-million dollar claim, sitting in KPC’s and its advisers’ inboxes weeks before the offer closed, was carried into the disclosure documents with the specificity investors were entitled to expect.

That is a question for Faida Investment Bank, as the bank that earned an estimated KSh1.06 billion success fee for shepherding this transaction, and for TripleOKLaw and G&A Advocates, who under Appendix IV of the Information Memorandum gave their written consent to the legal opinion included in the offer document and authorised its contents. Neither firm has yet issued a public response to the questions raised on social media, and KPC’s own announcement does not address the IPO disclosure question at all, confining itself to the new suit and the standard caution to shareholders.

A COMPANY ALREADY UNDER SIEGE

The Zakhem claim does not land on a quiet company. It lands on a state enterprise whose post-listing months have been turbulent by any measure.

On April 2, 2026, barely three weeks after KPC’s shares began trading, the company’s substantive Managing Director, Joe Sang, was arrested alongside Petroleum Principal Secretary Mohamed Liban and Energy and Petroleum Regulatory Authority Director General Daniel Kiptoo over allegations tied to the importation of a substandard fuel consignment aboard the tanker MT Paloma.

All three resigned within days, in what State House described as a response to “egregious misrepresentation” in the petroleum supply chain. Pius Mwendwa, KPC’s General Manager for Finance, was named acting Managing Director, with the board moving quickly to reassure shareholders that operations remained stable.

It was, by multiple accounts, Sang’s second brush with the DCI. He had previously been charged, and later acquitted for lack of evidence, in connection with the Sh1.8 billion Kisumu Oil Jetty contract saga, a case that also implicated other senior KPC officials of that era.

For a company barely out of the IPO gate, the optics are difficult to overstate. Within one financial quarter of listing, KPC has had to disclose the arrest and resignation of its chief executive over a fuel quality scandal, and now a near eleven billion shilling lawsuit from a contractor whose claims against the company stretch back over a decade. Retail investors who bought into the narrative of a stable, cash generative monopoly are entitled to ask whether the picture painted for them in January was the full one available at the time.

WHAT THIS MEANS FOR THE MARKET

The immediate market consequence is the one KPC itself has flagged: heightened uncertainty around the counter, and a formal caution to shareholders dealing in the stock.

Beyond that, the Zakhem claim and its predecessors illustrate a pattern that ought to concern anyone underwriting Kenyan state enterprise valuations going forward.

The interest component of the new claim, at over USD65 million against a principal claim of just over USD19 million, is the clearest illustration of what happens when contractual disputes with international counterparties are allowed to run for years through Kenya’s courts while the meter keeps running at 14 percent annually.

The same dynamic is visible in the smaller, already-litigated USD6.03 million residual claim from the 2020 decree, where interest alone had grown to outstrip the underlying principal balance several times over.

If KPC ultimately loses or settles even a portion of the new USD84.1 million claim, the financial hit will not fall on the Government of Kenya, which retained 35 percent of the company and pocketed the bulk of the roughly KSh106 billion raised in the IPO. It will fall on the balance sheet of a company in which 70,000 ordinary Kenyans, alongside institutional and diaspora investors, now hold a direct stake.

For Faida Investment Bank and the joint legal advisers, the reputational stakes extend well beyond this single transaction. Kenya’s privatisation programme, of which the KPC IPO was the flagship and the first major test in nearly two decades, depends on investor confidence that the due diligence behind these offers is rigorous and that material risks are surfaced before, not after, the public is asked to buy in.

A credible, documented answer to the question Mwango Capital and Paras Shah have posed, specifically, what the January 2026 Information Memorandum said about Zakhem and when the advisory team became aware of the February 2026 demand letter, is now squarely in the public interest.

KPC has said it intends to defend the new suit vigorously and has briefed its advocates accordingly. The Commercial and Tax Division of the High Court will, in time, determine whether Zakhem’s USD84.1 million claim succeeds. But for the advisers who took home hundreds of millions of shillings in fees to bring KPC to market, and for the regulators who signed off on the offer documents, the more immediate reckoning may be the one playing out in public, where investors are asking, with increasing impatience, exactly what they were told, and what they were not.

This newspaper has sought comment from Faida Investment Bank, TripleOKLaw Advocates and G&A Advocates LLP on the specific question of how the Zakhem litigation history and the February 2026 demand letter were treated in the Information Memorandum’s risk disclosures, and will publish their responses in full if and when they are received.

Kenya Insights allows guest blogging, if you want to be published on Kenya’s most authoritative and accurate blog, have an expose, news TIPS, story angles, human interest stories, drop us an email on [email protected] or via Telegram

8 Dead After US Air Force B-52 Bomber Crashes Shortly After Takeoff In California

Sh11 Billion Zakhem Debt Bombshell Rocks Kenya Pipeline Three Months After IPO, As Questions Mount Over What Investors Were Told

How A Convicted Zimbabwean Fraudster Quietly Bought His Way Into Kenya’s Sh375 Billion JKIA Mega-Deal

How an Egyptian-Headquartered AI Medical Platform Harvested the Sensitive Health Data of Over 60,000 Kenyans — Leaving Thousands Exposed to a Mega Privacy Catastrophe in Foreign Hands

Inside the Cover-Up: How Diageo and EABL Allegedly Buried a Sexual Harassment Scandal at the Kisumu Brewery and Are Now Racing to Sell the Evidence Out of Kenya’s Reach

Lopokoiyit The Fraudster? Why A Past Scandal At Safaricom Has Come To Haunt Absa Executive Sitoyo

FACTBOX – Key Provisions In Iran-US Draft Memorandum Of Understanding According To Iranian Media

FACTBOX – What Sanctions Could Be Lifted Under New US-Iran Peace Deal?

Politician Charged in Court for Defrauding Couple Sh1 Million in Botched Deputy President’s Office Tender Deal

The Chairman’s Conflicts: How Adil Khawaja’s Boardroom Empire Compromised Safaricom’s Governance

Inside NCBA’s Decline: How a Banking Giant Lost Its Strategic Edge

Cement, Cash and Courts: How the Hashu Dynasty Crushed the Ramji Brothers for Fourteen Years and Why the Walls Are Now Closing In

Standard Chartered Ghosts Haunt Joshua Oigara At Stanbic As Whistleblower Spills Beans

Inside The Urban Planning Cartel That Owns Nairobi

Businessman Philip Waithaka Kinuthia’s Minor Son Allegedly Drove Drunk, Killed Two Peponi Students in Ngong Road Horror Crash as Claims of Cover-Up Intensify

South Sudan: Adut Salva Kiir’s Shadow Treasury Exposed

Why Ruto’s Favourite Candidate Adan Mohammed Could Be Locked Out of the KRA Top Job

Why John Ngumi Is Running From the EACC and Why the Sh415 Million Payday May Be the Least of His Worries

Betika Faces DCI Probe, Directors Arrest and License Revocation Over Massive 29.5 Million Safaricom Customers’ Data Breach

The President’s Daughter and The Missing Witness: How Adut Salva Kiir’s Shadow Treasury Silenced Its Most Dangerous Critic

-

Business6 days ago

Business6 days agoInside NCBA’s Decline: How a Banking Giant Lost Its Strategic Edge

-

Investigations2 weeks ago

Investigations2 weeks agoCement, Cash and Courts: How the Hashu Dynasty Crushed the Ramji Brothers for Fourteen Years and Why the Walls Are Now Closing In

-

Business5 days ago

Business5 days agoStandard Chartered Ghosts Haunt Joshua Oigara At Stanbic As Whistleblower Spills Beans

-

Investigations1 week ago

Investigations1 week agoInside The Urban Planning Cartel That Owns Nairobi

-

News20 hours ago

News20 hours agoBusinessman Philip Waithaka Kinuthia’s Minor Son Allegedly Drove Drunk, Killed Two Peponi Students in Ngong Road Horror Crash as Claims of Cover-Up Intensify

-

Africa4 days ago

Africa4 days agoSouth Sudan: Adut Salva Kiir’s Shadow Treasury Exposed

-

Business4 days ago

Business4 days agoWhy John Ngumi Is Running From the EACC and Why the Sh415 Million Payday May Be the Least of His Worries

-

Africa5 days ago

Africa5 days agoThe President’s Daughter and The Missing Witness: How Adut Salva Kiir’s Shadow Treasury Silenced Its Most Dangerous Critic