Investigations

How Bangled KENYATTA NATIONAL HOSPITAL PROCUREMENT OF INSURANCE SERVICES Bid Rigging Unfolded and How PPRA Is Protecting Jubilee Insurance In Coverup.

More information from our source – the whistleblower continues to unfold the rot in the Procurement industry with the help of PPRA-PPRB the procurement authorities. The corrupt Jubilee Insurance Co / Jubilee Allianz General Insurance Co king of kickbacks colluding with the authorities to win tenders through rigging – birds of the same feathers flocking together.

“BID RIGGING AND CORRUPTION IN KENYATTA NATIONAL HOSPITAL PROCUREMENT OF INSURANCE UNDERWRITING SERVICES – KNH/T/46/2021-2022

Good morning,

We plead for your keen attention on the matter referenced. KNH advertised for the above tender that closed on 8/6/2021. We will clearly outline how the whole scandal chronologically unfolded. All the information given here is the actual status on the ground and is verified and verifiable. We again state that we have and will continue to observe professionalism, ethics and objectivity throughout the matter.

PRIOR TO ADVERTISEMENT

KNH had running contracts with CIC Life Assurance Ltd for Group Life Cover. The same tender included other classes of general insurance which were awarded to other companies. The tender was advertised in 2019 and awarded with no challenges. Contracts were to run for two yertas: 201-2020 and 2020-2021, commencement date being April 2019 and end date March 2021. We have however established that, just before the end of the contracts, KNH extended the contracts by three months from March 2021 to June 2021. According to the Professional Opinion seen by us that was recommended to the CEO by the Head of Procurement for approval signed in March 2021, justification for the three months extension was so as to align the contract period with the financial year. KNH has several contracts for adverse services including security, cleaning, gardening services among others whose start and end dates are not aligned with the financial year shenanigan. How these insurance services contracts were the only one sensitive to the financial year period cannot be explained.

After the extension, the journey of preparing for advertisement of the new tender began. Our investigations have revealed that the new items in question were introduced by people in the insurance industry who were involved in preparation of the tender document. Two underwriters and an agent who exposed the KNH staff without knowing convinced KNH to include the items as mandatory in the tender document. One tender document was prepared combining both Group Life business and the general business.

Group Life business is where the turpitude and depravity is. Unknowingly, KNH was lured into adopting the scandalous criteria and blindly putting the same in the tender document. The criteria demanded that the underwriter must have made 100Million profit for the last three years and Gross premium of 500M for the year 2020 as per IRA reports. When the IRA reports are analysed, only one company Jubilee Life Assurance Limited meets the two criteria for Life business. This was done intentionally so as to lock all other life business underwriters. See the analysis below:

The figures are derived from the IRA reports as was required in the tender document.

| Insurance Co. | 2020 | 2019 | 2018 |

| APA Life Assurance Company | 115,843, 000 | 28,684, 000 | (66,752, 000) |

| ICEA Lion Life Assurance | 774,360, 000 | 690,245, 000 | 600,295, 000 |

| Jubilee Insurance Company | 1,197,880, 000 | 2,198,267, 000 | 1,408,505, 000 |

| Liberty Life Assurance Company | 273,016, 000 | 478,613, 000 | 283,311, 000 |

| Sanlam Life Assurance | 649,621, 000 | – | – |

| Britam Life | (2,207,207, 000) | 4,213,789, 000 | (960,370, 000) |

| Old Mutual Life Assurance | (346,154, 000) | 175,825, 000 | 480,732, 000 |

| Pioneer Assurance Company | (60,645, 000) | 142,288, 000 | (35,258, 000) |

| UAP Life Assurance Company | (532,751, 000) | 219,708, 000 | 251,120, 000 |

According to the above analysis, only three (3) Life underwriters will have made profits for the three years required and will pass criteria number 12. These are: Jubilee Insurance Company, Liberty Life Assurance Company and ICEA Lion Life Assurance. Criteria no. 13 for life underwriters required that the life underwriter should have gross premiums of Kshs. 500Million. Analysis of the three (3) underwriters who pass criteria no. 12 have the following Gross premiums indicated against their names:

names:

| Insurance Co. | Gross underwritten premiums |

| Jubilee Insurance Company | 704,881, 000 |

| Liberty Life Assurance Company | 376,687,000 |

| ICEA Lion Life Assurance | 326,242,000 |

Going by the analysis given above, it’s worth noting that only Jubilee Insurance Company can meet the two mandatory requirements in the market. It’s in the same that we conclude that the tender document was customized to ONLY allow Jubilee Insurance Company and no other company whatsoever to qualify for the life business. This is despite the fact that Kenya has close to thirty (30) underwriters registered for Life Business.

AFTER ADVERTISEMENT

Several insurance companies had noticed the presence of the malicious criteria in the tender document. The companies went ahead and made enquiries requesting for revision of the mandatory requirement that formed the preliminary evaluation criteria. The companies include: Britam, Liberty, Metropolitan Canon, Kenindia and Sanlam. KNH ignored all the queries and concerns raised and never responded to any of them. They were quickly printed by the office of the Director Supply Chain Management and deleted from the email, probably assuming that the same will be deleted from the senders’ emails. Other stakeholders including agents also complained of the criteria. No response was given at all but rather promised to deal with the consequences irrespectively. Reasons why the same were included in the tender document have never been given upto now. There’s no basis at all for the profitability criteria and neither the procurement laws nor insurance nor Public Finance laws support the same. It’s therefore illegal in its mentioning.

Section 55 of the Public Procurement and Asset Disposal Act, 2015 on eligibility to bid states that a person is eligible to bid for a contract in procurement only if the person satisfies the following criteria:

(a) the person has the legal capacity to enter into a contract for procurement or asset disposal; (b) the person is not insolvent, in receivership, bankrupt or in the process of being wound up; (c) the person, if a member of a regulated profession, has satisfied all the professional requirements; (d) the procuring entity is not precluded from entering into the contract with the person under section 38 of this Act; (e) the person and his or her sub-contractor, if any, is not debarred from participating in procurement proceedings under Part XI of this Act; (f) the person has fulfilled tax obligations; (g) the person has not been convicted of corrupt or fraudulent practices; and (h) is not guilty of any serious violation of fair employment laws and practices.

We were not able to trace where profitability lies in the above.

TENDER CLOSING

During tender closing/ opening, it was noted that one bidder, Geminia Insurance Limited submitted one composite document meaning that the financials attached in the tender document were for the composite company and not for the subsidiary company. All the other bidders separated the life business financials from general financials and submitted the bid documents separately. For instance, Jubilee Life Assurance Ltd submitted a separate bid from Jubilee General Insurance Ltd.

TENDER EVALUATION

DURING TENDER EVALUATION, THE COMMITTEE NOTICED THAT THERE WERE ISSUES IN THE TENDER DOCUMENT. They immediately wrote to the office of the Head of Procurement requesting for clarification and professional advice on how to manoeuvre with the evaluation. The issues raised were:

- That the criteria on 100Million profitability for the year 2020 was not objective but rather subjective since, under Life business, only one bidder passed and therefore making it not competitive, which would mean that more stable and competitive bidders were locked out of the tender.

- The issue of Geminia Insurance who submitted composite financials. The head of procurement was requested to advise on how the bidder would be evaluated among others.

- The tender document requested for Gross Premium. How to calculate the gross premium was given in the tender document and therefore the item was ambiguous.

Instead of officially responding to the tender evaluation queries, the management influenced the committee to ignore the issues raised and proceed to award to the already pre determined awardees. The report was rushingly done, forwarded after working hours, professional opinion done at the same time and approved at night of the same day when all other staff had left the hospital so as to leave the other staff unaware of what was happening.

During evaluation, we contacted KNH in effort to plead for a response but they continually ignored our concerns. At one point before the tender closed, when an underwriter visited the procurement offices, he was kept waiting for five hours and later gave up and left.

AFTER AWARD

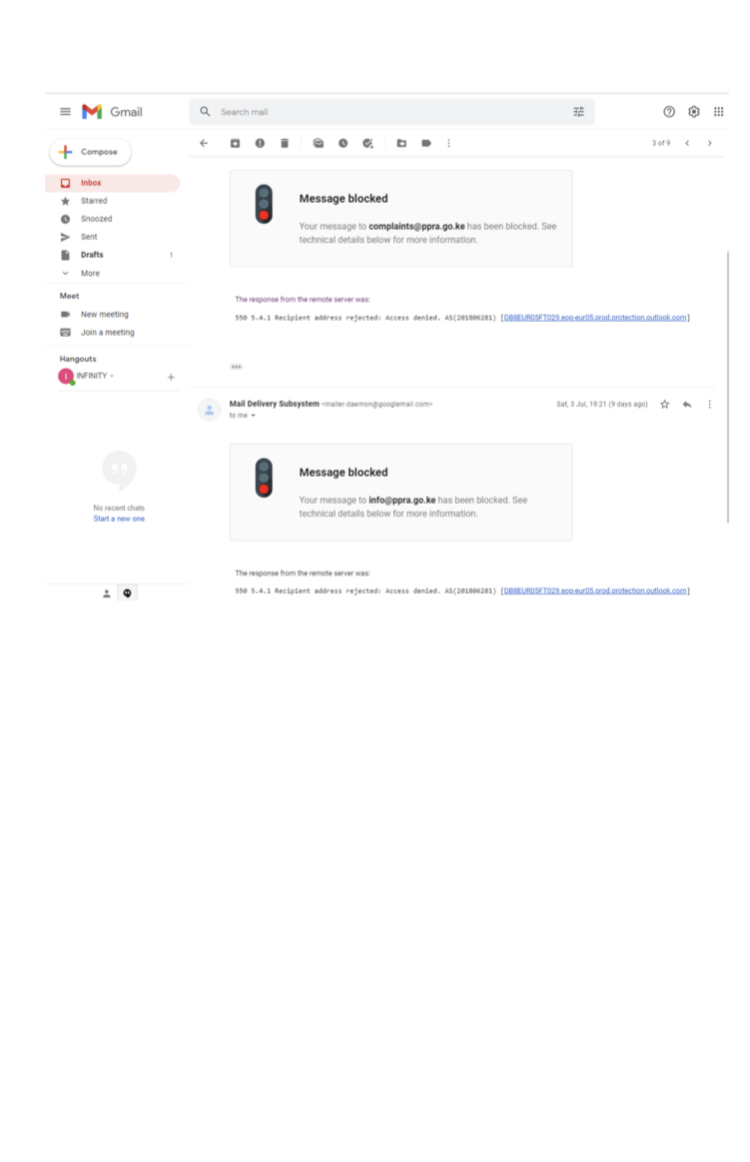

We made several complaints to both KNH and PPRA. None was responded to. We realized that KNH had promised both ther agent involved and the bidders in question that they would control the situation and not bother with the complaints. CIC Life Assurance Ltd challenged the procurement process at PPRA on 24th June 2021 exactly ten days after the tender award. KNH signed the letters of award on 14th June 2021. PPRA has never responded to the issues raised . We made several complaints subsequently but both parties played dumb. Public offices are put in place for a purpose and public officers should conduct their duties ethically and professionally.

In an effort to water down the issues raised and counter our complaints as their way of cooling down the heat, KNH management and the agent who choreographed the scandal agreed to form a pseudo mail account and masquerade as a concerned underwriter and purport that we are following up on the same because we are paid to do to so and that our concerns are baseless and aims at tainting the name of the hospital. They also negotiated with PPRA and requested PPRA to block all emails coming from us.

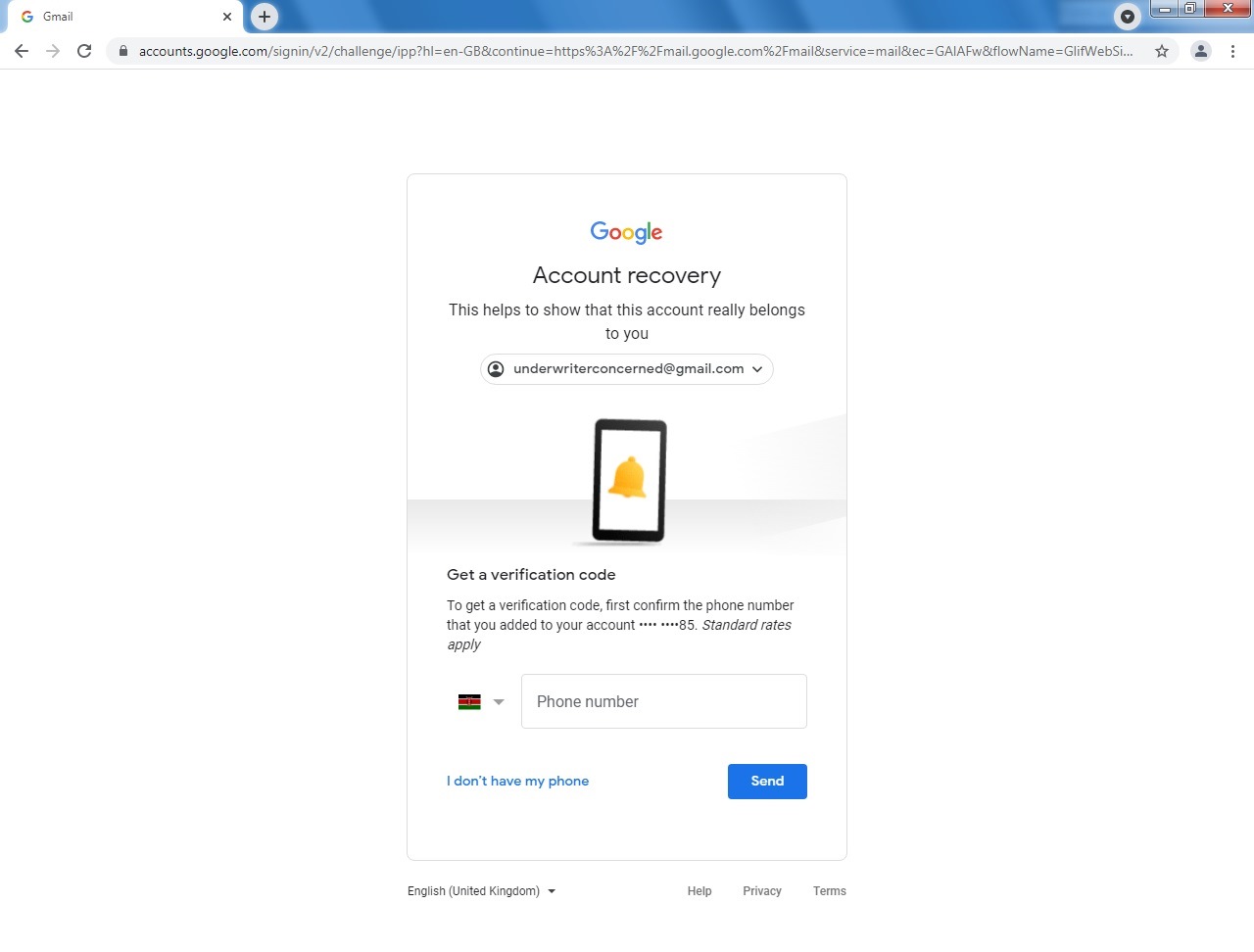

The email was created on 5th July 2021: [email protected]. This is the email used to counter our complaints and arrogantly respond to us, whose responses are equivocal and scanty hogwash.

This has prompted our investigations to go a notch higher and we can now authoritatively report that google gurus are on it. Preliminary investigations have unearthed that, according to google coordinate protocols, the email address used i.e [email protected]was registered with this safari.comnumber, 0722***585

This number after investigations belongs to a kenyan in the insurance industry who is a registered agent, one that we’ve constantly mentioned to be the choreographer and mastermind of the scandal and is involved in several others in the government including The Youth Fund that previously led to the dismissal of the former head of procurement. The number is also traced with some KNH officers in sports clubs, parking lots and some residential places before, during and after the tender. We however note that the parties have now opted to communicate via whatsapp in fear of being tracked.

We are in the assignment of getting more information and profiles of the parties involved and will be back with more information. We won’t expose all the details at this stage.

We request that you take the matter seriously so as to stop the impunity and scam in KNH and the insurance industry.

Regards.

On Thu, 1 Jul 2021 at 18:16,To Director,Public Procurement Regulatory AuthorityAttention: PPRBGood evening,We wish to come to you once again in regards to the same subject matter. All the issues raised in our previous correspondences have never been addressed by the procuring entity and no response whatsoever has ever been given to us. We feel that this is impunity and lack of respect to stakeholders and the state at large.Kindly note that we raised the issues way before the tender closed. It’s now three (3) weeks plus and still counting. It’s worth noting that the main issue was and still is the criteria that was maliciously introduced in the tender documentby KNH (Kenyatta National Hospital) for the tender for Procurement of Insurance Underwriting Services, KNH/T/46/2021-2022. The criteria read “The underwriter must have a gross profit of 100million each year for the last 3 years (2020, 2019 & 2018) as per IrA reports.We have previously indicated that the same was introduced after a meeting that the KNH bosses had with senior officers in Jubilee Life assurance Ltd who were introduced to each other by an insurance agent (who is related to the Head of Procurement in KNH and come from the same place)and have previously fixed several deals together according to the agent), and who lured them into introducing the criteria so as to knock out all other bidders in Life underwriting services and only pave way for Jubilee Life assurance Ltd who would later win the said tender. We will not mention names for now.We requested KNH to provide the legal basis that supports this criteria and upto now they have never responded. They ignored all our concerns and never issued any addendum, but went ahead and awarded the tender. All the queries went unanswered.The general definition of Gross Premium is “The revenue of a company after it accounts for what had to be paid out to return that revenue, meaning it is the amount of money actually earned. How to calculate gross profit: Gross Profit = Total Revenue – Total Cost. IRA reports only provide for Profit before tax and profit after tax. How this issue was treated in the tender evaluation remains a mystery.It’s in the public domain that KNH bosses have assured the agent and the underwriter who was awarded the Life Insurance business that they will handle PPRB staff and that no complaint will be successful. As of now, we are aware that CIC Life Assurance Co. Ltd have already challenged the procurement process with PPRA/Public Procurement Review Board (PPRB) and we are equally aware that KNH bosses who have their cuts already negotiated and assured are working day and night to influence the decision of the Review board, and that they are rushing to sign the contracts so that payment can be done urgently even as complaints are put every day.We kindly request for your urgent action so as to end the impunity and outright corruption.Regards,

On Sun, 27 Jun 2021 at 20:45,

AttentionDIRECTOR,PPRA & PPRBWe report to you the above subject matter whereby KNH (Kenyatta National Hospital) advertised for Procurement of Insurance Underwriting Services, KNH/T/46/2021-2022 on 27th May 2021 that closed on 08/06/2021. We noted that two items in the tender document and specifically the qualifying threshold for Life underwriting business (page 24 of the tender document) were intentionally introduced in the tender document for this year so as to only allow one underwriter, who is the only one who meets the threshold to qualify for the tender. The items are:

1. Preliminary criteria no. 12 , The underwriter must have a gross profit of 100million each year for the last 3 years (2020, 2019 & 2018) and,2. Preliminary criteria no. 13 life underwriters must have gross premiums of Kshs. 500Million for the year 2020.The item of profitability coupled with Gross premium of Kshs. 500 Million were put as mandatory in the tender document to lock out all other Life business underwriters and only allow Jubilee Life assurance Ltd win the tender.Section 55 of the Public Procurement and Asset Disposal Act, 2015 on eligibility to bid states that a person is eligible to bid for a contract in procurement only if the person satisfies the following criteria:(a) the person has the legal capacity to enter into a contract for procurement or asset disposal; (b) the person is not insolvent, in receivership, bankrupt or in the process of being wound up; (c) the person, if a member of a regulated profession, has satisfied all the professional requirements; (d) the procuring entity is not precluded from entering into the contract with the person under section 38 of this Act; (e) the person and his or her sub-contractor, if any, is not debarred from participating in procurement proceedings under Part XI of this Act; (f) the person has fulfilled tax obligations; (g) the person has not been convicted of corrupt or fraudulent practices; and (h) is not guilty of any serious violation of fair employment laws and practices.

As we have previously indicated, these two items in question were introduced by an agent in agreement with the underwriter who convinced KNH bosses after discussing their share.The same agent is lying to unsuspecting accounting officers and Heads of Procurement who seem not to properly understand the insurance business and at times, misadvising them on matters insurance which later backfires and leaves them in serious problems. The Fact of the matter is that the items are unlawful and contravene the provisions of all the procurement, public finance and insurance laws. Eligibility of tenders is clearly and precisely outlined in the above mentioned section 55 of the procurement Act.

We would also want to bring to your attention that the same issues were raised by the KNH Tender Evaluation Committee who noticed the weirdness of their inclusion into the tender document. The committee would immediately write to the Head of Procurement requesting for guidance on how to handle them since they were very subjective and locked out all the other bidders in the Life business.

The issues raised by the evaluation committee were not responded to but instead the committee was silenced and assured of their share. Other members of the committee who tried to enquire further were intimidated and blackmailed.

It’s also worth noting that we, and other insurance stakeholders raised these issues way before the tender closed. Underwriters, also, some of whom participated and others who chose not to participate in the tender, also raised issues both in soft and in print. All those issues and queries raised were ignored and went unanswered. Negligence and lack of professionalism at the highest.As at now, the tender has already been awarded and KNH chose to communicate to all other bidders who participated and leave out the current service provider so that they may NOT know the results and therefore fail to challenge the procurement process with the Procurement Review Board: the window of which expires tomorrow 28/06/2021.The issues of negligence highlighted are so unfortunate and we call upon the authority and all other regulatory bodies to take the matter seriously and deal with the scam once and for all.Thank you in advance for your consideration.Regards,”

Kenya Insights allows guest blogging, if you want to be published on Kenya’s most authoritative and accurate blog, have an expose, news TIPS, story angles, human interest stories, drop us an email on [email protected] or via Telegram

Netanyahu Says Israel Must ‘Break Free from Dependence’ After Tensions With Trump Administration

Niger pulls Out Of International Criminal Court After Calling It Neo-Colonialist

Kenya Awards Sh154 Billion JKIA Upgrade Tender To Chinese Firm CRBC

The Untouchable: How KURA’s Silas Kinoti Has Survived A Decade Of Corruption Storms While Kenya’s Roads Bled

Fake Papers, Dirty Millions And The Analo Connect: How Kitisuru MCA Alvin Palapala Built a Shadow Empire Inside Nairobi’s Planning Machine

Migori Payment Row Deepens As Branding Firm Demands Sh3.8 Million Over Unpaid Piny Luo Festival Deal

Utumishi Girls Fire Suspects To Be Charged With Murder

Putin Says Russia Ready For Peace Talks With Ukraine Based on Anchorage, Istanbul Agreements

South Sudanese Must Give Adut Salva Kiir The Benefit Of The Doubt

Kenya Stops Work At The US-Linked Ebola Facility

Businessman Philip Waithaka Kinuthia’s Minor Son Allegedly Drove Drunk, Killed Two Peponi Students in Ngong Road Horror Crash as Claims of Cover-Up Intensify

Inside NCBA’s Decline: How a Banking Giant Lost Its Strategic Edge

South Sudan: Adut Salva Kiir’s Shadow Treasury Exposed

Cement, Cash and Courts: How the Hashu Dynasty Crushed the Ramji Brothers for Fourteen Years and Why the Walls Are Now Closing In

Standard Chartered Ghosts Haunt Joshua Oigara At Stanbic As Whistleblower Spills Beans

Inside The Urban Planning Cartel That Owns Nairobi

THE VULTURE AND THE SCHEME How Nairobi West Hospital Became the Most Dangerous Institution in Kenya’s SHA Ecosystem and Why the Books Must Be Audited Now

The President’s Daughter and The Missing Witness: How Adut Salva Kiir’s Shadow Treasury Silenced Its Most Dangerous Critic

How Adil Popat Saved His Empire On The Eve Of Imperial Bank Collapse and Why Kenya’s Mainstream Media Buried The Story

Why John Ngumi Is Running From the EACC and Why the Sh415 Million Payday May Be the Least of His Worries

-

News1 week ago

News1 week agoBusinessman Philip Waithaka Kinuthia’s Minor Son Allegedly Drove Drunk, Killed Two Peponi Students in Ngong Road Horror Crash as Claims of Cover-Up Intensify

-

Business2 weeks ago

Business2 weeks agoInside NCBA’s Decline: How a Banking Giant Lost Its Strategic Edge

-

Africa2 weeks ago

Africa2 weeks agoSouth Sudan: Adut Salva Kiir’s Shadow Treasury Exposed

-

Business2 weeks ago

Business2 weeks agoStandard Chartered Ghosts Haunt Joshua Oigara At Stanbic As Whistleblower Spills Beans

-

Investigations5 days ago

Investigations5 days agoTHE VULTURE AND THE SCHEME How Nairobi West Hospital Became the Most Dangerous Institution in Kenya’s SHA Ecosystem and Why the Books Must Be Audited Now

-

Africa2 weeks ago

Africa2 weeks agoThe President’s Daughter and The Missing Witness: How Adut Salva Kiir’s Shadow Treasury Silenced Its Most Dangerous Critic

-

Business2 weeks ago

Business2 weeks agoHow Adil Popat Saved His Empire On The Eve Of Imperial Bank Collapse and Why Kenya’s Mainstream Media Buried The Story

-

Business2 weeks ago

Business2 weeks agoWhy John Ngumi Is Running From the EACC and Why the Sh415 Million Payday May Be the Least of His Worries